Now more than ever, ASIC is moving against SMSF auditors who are in breach of the independence rules & for not performing a quality audit, including not obtaining sufficient appropriate audit evidence (not obtaining external confirmations to support the audit evidence - Auditing Standard of Australia 505).

If you do not know what is ASA 505, you are not alone - all those disqualified SMSF Auditors also did not know !

What happens when checking Market Valuations as per SIS R 8.02B

Supply of all audit evidence of the fund to the auditor is the responsibility of the Trustee. However, in the real world, as the auditor is referred by the Accountant, all audit evidence are usually provided by them without the Trustee personally getting involved.

Hence, when ATO / ASIC audits the auditor and blames them for not obtaining sufficient appropriate audit evidence, it is basically the accountant not supplying what the auditor needs - reversely - it is the auditors fault for not seeking the relevant audit evidence from the accountant.

No matter which way you look at it - since not sufficient audit evidence is gathered - it means that if an independent auditor looks at the auditors file and cannot reach at the same conclusions based on the audit evidence collected by the original auditor - the auditor who audited the fund is in trouble with the ATO.

Technically, if your audit file cannot be relied on, with all the surrounding evidence which makes up the financial statements and if all the available audit evidence in your file are not sufficient as per ATO's scrutiny - ATO will refer you to ASIC recommending that you be disqualified or additional conditions be put on your auditors registration.

Without back tracking whose fault it is - the SIS Act prevents the SMSF auditor to issue an unqualified report where there is a misstatement in the financial statements and / or that misstatement is not communicated to the Trustee and to the regulator.

One such assertion in the financial statements is market value of ASX share price and dividends income of the fund. Before we dig deep into what actually happens in real life and where the auditor needs to be cautious, lets look at the auditing standards first - ASA 505

ASA 505 External Confirmation Procedures to Obtain Audit Evidence

Paragraph 2: ASA 500 indicates that the reliability of audit evidence is influenced by its source and by its nature, and is dependent on the individual circumstances under which it is obtained. That Auditing Standard also includes the following generalizations applicable to audit evidence

- Audit evidence is more reliable when it is obtained from independent sources outside the entity.

- Audit evidence obtained directly by the auditor is more reliable than audit evidence obtained indirectly or by inference.

- Audit evidence is more reliable when it exists in documentary form, whether paper, electronic or other medium"

Accordingly, depending on the circumstances of the audit, audit evidence in the form of external confirmations received directly by the auditor from confirming parties may be more reliable than evidence generated internally by the entity. This Auditing Standard is intended to assist the auditor in designing and performing external confirmation procedures to obtain relevant and reliable audit evidence.

Evaluating the Evidence Obtained

Paragraph 16. The auditor shall evaluate whether the results of the external confirmation procedures provide relevant and reliable audit evidence, or whether further audit evidence is necessary.

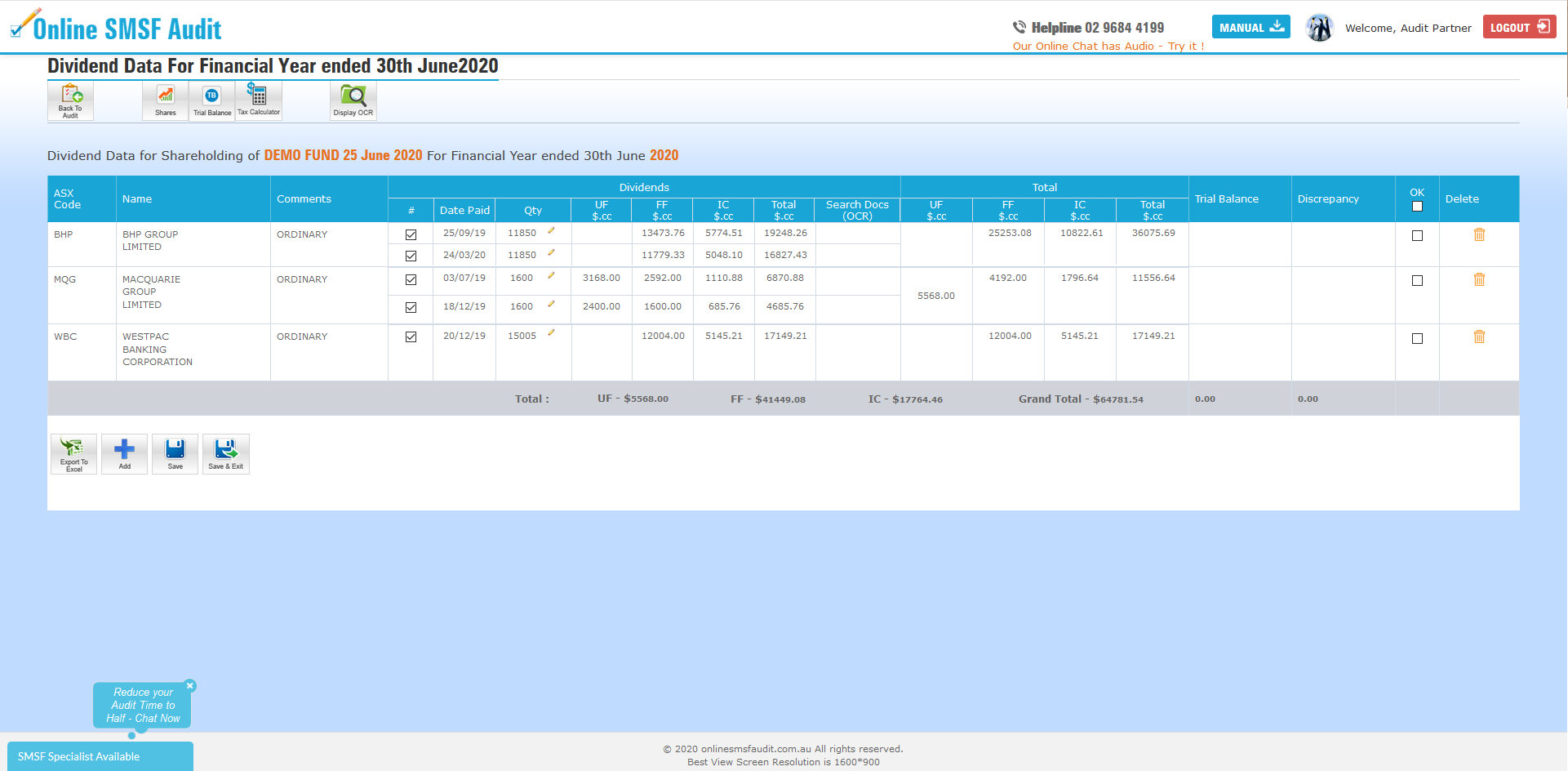

Real World : What is given to the Auditor as Audit Evidence whilst checking Closing share prices and Dividend Data

Lets consider the risks, last week, ASIC moved against two auditors who breached the independence rules and for not obtaining sufficient appropriate audit evidence. ASIC asked them to attend additional training on SMSF audits & ethics after which they also need to sit and pass the SMSF auditor competency exam.

In the context of market value of shares

SISR 8.02B: For subsection 35B(2) of the Act, for the year of income 2012–13 and any later year of income, when preparing accounts and statements required by subsection 35B(1) of the Act, an asset must be valued at its market value.

The auditor will usually get a listing of shares which the fund owns with market value from the share trading platform where the fund has a share trading account. If the accountant prepare financials statements on an online accounting package then perhaps an investment report which the software spits out, determining closing prices and dividends declared.

ATO will probably not consider these documents as sufficient - as the auditor has not confirmed the figures from an external source and may also consider the auditor's procedure as not reliable and hence not worthy to form an audit opinion due to lack of external party confirmations in his audit procedures.

How does the Audit procedure on Online SMSF Audit fulfills this requirement

We are the only online SMSF audit software which feeds in the software closing share prices and annual ASX dividend data which we source independently. The table which the software generates (see below) becomes an external confirmation that the auditor can rely and make audit conclusions.

This table forms a part of your working papers file which the ATO looks at while evaluating your audit quality.

If you are using another online SMSF audit software - please ensure as an auditor that you do not rely on the figures which the software provides as all accounting software allow the operator to change figures. Any closing shares prices provided by a trading platform of the fund cannot be relied upon conclusively.

This software has been designed by an ASIC Approved SMSF Auditor, Manoj Abichandani.

NEW APES 110 RULES on SMSF Auditor Independent Requirements

16th March 2021, 2:00 PM to 3:00 PM.

For booking the webinar, please go to our Webinar tab on the main website homepage.

New SMSF Audit Report is Online

Changes have been made to the Self-managed super fund independent auditor’s report (IAR) (NAT 11466-07.2019) effective for reporting periods starting on or after 1st July 2019. This form replaces the previous IAR that was effective for reporting periods on or after 1st July 2016. You must use the new form for reporting periods starting on or after 1st July 2019.

We will be discussing:

Circumstances when you Can & Cannot Audit a fund where Accounts are prepared by your firm

What auditors must do to protect to not breach the new Independence requirements

What changes you should make in your Accounting firm now to retain the audit work

FREE WEBINAR

To explain the changes in the Audit Report attend our free webinar

We continue to strive to make useful enhancements to the software to bring in more efficiency for auditors to carry out fully compliant audits effectively.

Should you want any additional feature, do not hesitate to contact me directly. Thank you for your continued support.

.jpg)