Minimum Pension Drawdown: Ensure Compliance Before 30 June

News | Mehak Gaba|Released: 07/04/2025 | Read: 3 Mins

Minimum pension drawdown refers to the mandatory percentage set by the government that retirees must withdraw each financial year to maintain the tax-exempt status of their pension. There is no maximum amount on withdrawals.

These rules are in place to ensure that superannuation savings are used to fund retirement—not left indefinitely in a tax-advantaged environment.

Regulations relating to minimum pension payments

In accordance with Regulation 1.06(9A) of the Superannuation Industry (Supervision) Regulations 1994, trustees must adhere to the following requirements for pensions that commenced on or after 1 July 2007.

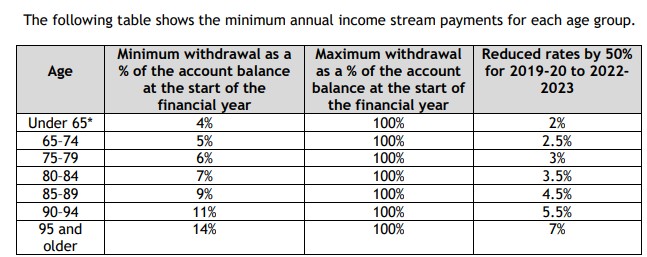

The minimum pension amount is determined based on the following criteria:

The member’s age – Different age brackets have different minimum percentage factors.

The account balance as of 1 July 2024 – This balance is used to calculate the minimum payment for the financial year.

A pro-rata calculation – Applies when a pension starts partway through the financial year, with the minimum payment adjusted based on the number of days remaining in that year.

How are the minimum pension payments calculated?

Case Study 1: The Impact of Age and Account Balance on Minimum Pension Payments

David is a 74-year-old retiree with $200,000 in an account-based super pension as of 1 July 2023.

Based on his age, David is required to withdraw 5% of his account balance by 30 June 2024, which amounts to aminimum pension payment of $10,000 ($2,00,000× 5%) for the 2023–24 financial year.

On 1 July 2024, the balance of David’s super pension has grown to $205,000.

As David turns 75 in the 2024–25 financial year, his required minimum drawdown rate increases to 6%. Therefore, he must now withdraw $12,300 ($205,000 × 6%) by 30 June 2025.

Minimum pension payment requirements vary based on the member’s age and the account balance at the start of the financial year.

Case Study 2: Lisa Starts Her Pension Mid-Year

Lisa Starting account balance of pension: $300,000

Member age: 67

Minimum annual percentage: 5%

Pension start date: 1 March 2025

Days remaining in the financial year: From 1 March 2025 to 30 June 2025 = 122 days

This means that, for the 2024–25 financial year, the member will be required to withdraw a minimum of $5,010 from their pension account before 30 June 2025.

Case Study 3: Michael Starts Late in the Year

Michael starts his account-based pension on 15 June 2025.

Because there are only 15 days left in the 2024–25 financial year, he is not required to make a minimum pension payment before 30 June 2025.

Instead, Michael's first required drawdown will fall in the 2025–26 financial year and must be made before 30 June 2026.

What Happens If You Fail to meet the minimum Pension requirements?

Pension Income Stream Deemed to Cease: If the required minimum amount is not fully paid by 30 June, the pension is deemed to have ceased on 1 July of that financial year — as per ATO Tax Ruling TR 2013/5 (Paragraphs 93–95). This is a retrospective taxation outcome, the pension is no longer treated as being in the retirement phase, even if some payments were made.

2. Loss of Exempt Current Pension Income (ECPI): Once the pension ceases, the SMSF loses its entitlement to claim ECPI on the assets supporting that pension. All earnings and capital gains generated by those assets during the year become fully taxable at 15%, significantly reducing tax efficiency.

3. Reclassification of Pension Payments: Any payments made from the pension account during the year are reclassified as lump sum withdrawals rather than pension income stream payments. This can lead to adverse tax consequences, especially for payments made from taxable preserved benefits.

4. TBA (Transfer Balance Account) Consequences: The pension is treated as ceasing at the point it becomes evident that the minimum standards were not met (usually at 30 June). A debit is recorded in the member’s TBA, equal to the pension’s value at cessation.

This may free up space under the transfer balance cap for future pensions.

However, it does not reverse any prior credits.

5.Lock-In of Tax Components: The proportion of tax-free and taxable components of the pension becomes fixed at the date of cessation. This locks in the tax treatment of future withdrawals and can restrict estate planning flexibility.

Can the ATO Provide Any Relief for Failing to Meet Minimum Pension Requirements?

While the consequences of failing to meet minimum pension requirements can be significant, the ATO does provide limited administrative relief under the Commissioner’s General Powers of Administration (GPA) — but only in specific circumstances.

Trustees may self-assess or apply for this exception if the following conditions are met:

The shortfall is minor — no more than 1/12th of the annual minimum pension amount.

The failure was due to an honest mistake or something outside the trustee’s control (e.g., technical errors, timing issues).

A catch-up payment is made as soon as practicable in the following financial year and is allocated back to the previous year via appropriate accounting entries.

⚠️ Important: Self-assessment is allowed once per trustee/fund. Any future failures must be dealt with via a formal application to the ATO.

Final Thoughts

Ensuring compliance with minimum pension standards is an essential responsibility for SMSF trustees. With increasing regulatory scrutiny and the significant financial consequences of non-compliance, it is critical to implement comprehensive pension monitoring systems. Regular, ideally quarterly or monthly, reviews will help ensure that all payments are made on time, documentation is accurate, and no deadlines are missed.

While the ATO’s General Powers of Administration (GPA) exception offers a valuable safety net for genuine oversights, it should not be treated as a fallback. Trustees must prioritize proactive management and compliance to avoid unnecessary risks and maintain the tax advantages of the retirement phase. Relying on the GPA exception should be reserved for rare circumstances, not as a regular solution.

Speak to your SMSF administrator or financial adviser now to ensure your pension obligations are met by 30 June.

Visit www.trustdeed.com.au for more details or call us on (02) 9684 4199

.jpg)