Fixed Unit Trusts & Land Tax Relief: A Compliance Guide for Accountants

News | Navjot Kaur |Released: 25/06/2025 | Read: 3 Mins

As trust structures become more common in investment and property arrangements, many clients are turning to Fixed Unit Trusts (FUTs). While these structures can provide both tax and asset management benefits, it's essential to understand that not all “fixed” trusts are recognised as such under tax law — and the implications can be significant, especially when tax losses are involved.

This guide outlines what accountants need to know when advising clients on Fixed Unit Trusts, particularly in the context of land tax relief and tax loss utilisation.

What Is a Fixed Unit Trust?

A Fixed Unit Trust is a trust in which beneficiaries (unit holders) hold defined and proportionate entitlements to the trust’s income and capital, based on the number of units they own. These rights must not be subject to the discretion of the trustee.

However, labeling a trust as “fixed” is not enough. Under Australian tax law, a trust must meet strict requirements to be treated as a fixed trust for income tax purposes.

Practical Tax Implications

1. Capital Gains Tax Discount: If trust assets are held for over 12 months, the 50% CGT discount can flow through to unit holders.

2. NSW Land Tax Relief: Under Section 3A of the Land Tax Management Act 1956 (NSW), a trust may be recognised as a “fixed trust” if unit holders are treated as the equitable owners of the land. This allows the land tax threshold to apply.

What Qualifies as a Fixed Trust?

To qualify as a fixed trust:

Beneficiaries must hold clearly defined rights to income and capital.

These rights must be indefeasible — not subject to change by trustee discretion.

Units must reflect real, proportional ownership and be valued at net asset value.

In contrast, Hybrid Trusts involve multiple unit classes or allow trustee discretion, making them unsuitable for fixed trust treatment under tax law.

Legal Challenges and ATO Guidance

The definition of a fixed trust was narrowed significantly following the case Colonial First State Investments Ltd v FCT [2011] FCA 16, where the court clarified that fixed rights must be indefeasible. In practice, this is a high bar, and many trust deeds do not meet it.

In response, the ATO released PCG 2016/D16, outlining factors it considers when exercising discretion to treat a trust as fixed. However, this guidance introduces subjectivity, and there is still no legislative certainty despite ongoing industry feedback.

Risks and Compliance Considerations for Accountants

Unit Valuation: If the trust deed permits units to be issued or redeemed at values other than fair market value (net asset value), the trust may fail fixed trust status tests.

Trust Deed Review: Always verify that the deed includes fixed entitlement clauses and avoids trustee discretion over distributions.

Client Communication: Inform clients that fixed trust status is not automatically guaranteed, even with a well-drafted deed, due to ATO discretion and case law interpretations.

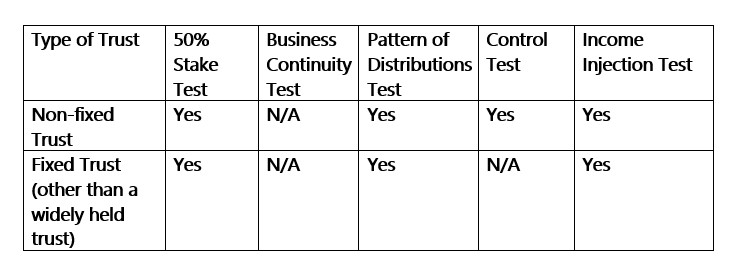

Trust Types and Tests for Loss Utilisation

Key Takeaways:

Non-fixed trusts must satisfy all four applicable tests, making loss utilisation more difficult.

Fixed trusts are only required to pass the 50% stake test and income injection test.

The pattern of distributions test and control test do not apply to fixed trusts (other than widely held trusts).

Action Steps for Accountants

For Existing Trusts:

Regularly review trust deeds to ensure compliance with current tax and land tax requirements.

Monitor unit ownership and stake changes to maintain fixed trust conditions.

For New Trusts:

Use deeds that are specifically drafted to maximise the likelihood of meeting fixed trust definitions.

Ensure units are issued at market value and all ownership rights are clearly documented.

For Trusts with Tax Losses:

Maintain detailed unit holder records.

Track ownership changes to ensure compliance with the 50% stake test.

Avoid any arrangements that could trigger the income injection test.

Conclusion

With the ATO and courts applying increasingly strict interpretations, achieving and maintaining fixed trust status has become a critical issue in trust and tax planning.

Accountants play a vital role in helping clients:

Choose the right trust structure,

Avoid compliance risks, and

Maximise available tax concessions.

Why Use Trustdeed’s Certified FUT Deed?

Trustdeed.com.au offers a certified Fixed Unit Trust Deed that meets the strict requirements of Section 3A of the Land Tax Management Act 1956 (NSW). This deed:

Has beenapproved by the NSW Office of State Revenueas a qualifying fixed trust deed

Allows trustees to access the , potentially saving thousands in annual land tax

land tax threshold

Visit www.trustdeed.com.au for more details or call us on(02) 9684 4199