💼 What is a TRIS (Transition to Retirement Income Stream)?

News | Mehak Gaba |Released: 17/07/2025 | Read: 5 Mins

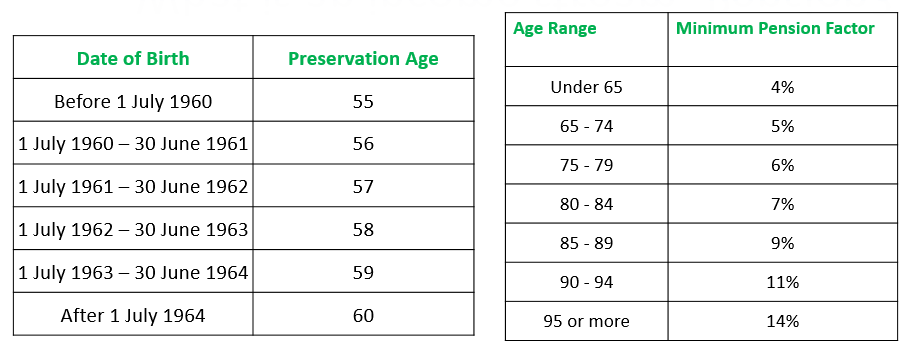

A Transition to Retirement Income Stream (TRIS) allows individuals who have reached their preservation age (currently age 60 for most people) to access a limited portion of their superannuation (SMSF). The preservation age is the minimum age a member can access their preserved super benefits without meeting another condition of release.

TRIS was Introduced in 2005 to support older Australians in gradually transitioning into retirement while remaining in the workforce. It enables continued employment (full-time or part-time) without needing to retire or leave their job.

Before the introduction of TRIS, members of SMSF could not access their superannuation unless they fully retired or met a limited condition of release. TRIS now offers flexibility by allowing access to part of your super while still actively working.

🔁Preservation Age by Date of Birth Minimum Pension Factor

Each financial year, you must withdraw between 4% (minimum) to10% (maximum) of your TRIS account balance. These limits are re-calculated annually based on your account balance as at 1 July.

🚨 Failure to withdraw minimum pensions of 4%

The ATO has adopted a stricter interpretation of pension rules within SMSFs. The failure to meet the minimum pension drawdown (4%) will now have serious tax and compliance consequences.

Key impacts include:

The pension is considered to have ceased from 1 July, not year-end.

The balance reverts to accumulation phase, and earnings become taxable.

Any existing accumulation accounts will merge, possibly disrupting estate and tax strategies.

The pension can only restart once the member rectifies any errors, such as failing to meet minimum pension drawdown requirements, which may take 13 to 22 months from the date the pension has to be commuted.

⚠️ Important Note:

The minimum 4% pension requirement is pro-rated based on how many days are left in the financial year when you start your Transition to Retirenment Income stream (TRIS).

For example, if you start a TRIS on 1 January, you’re only required to withdraw a portion of the 4% specifically, for half the year. However, the maximum is not pro-rated. So even if you start pension on 1 January, you can still access up to the full 10% of your balance for that financial year.

Is it is compulsory for your SMSF members to offer TRIS?

It's not compulsory for your SMSF to offer members a TRIS, although your SMSF may pay a TRIS, if the fund's trust deed allows this. However, your SMSF can pay a TRIS, if the fund’s trust deed permits it. If you wish to commence a TRIS but your current trust deed does not allow for it, you can update your trust deed using our platform.

How TRIS works- Step-by-Step?

You reach preservation age: You can start a TRIS once you hit your preservation age (depending on your birth year).

You move some or all of your super into a TRIS account: You don’t get a lump sum—you transfer part of your super to a TRIS account inside your fund.

You start receiving regular income: You must take out at least a minimum % (e.g. 4%) of your balance per year and cannot take out more than 10% per year (unless you fully retire).

TRIS payments are taxed: Earnings are taxed at a maximum of 15 % within a TRIS in non-retirement phase, while earnings are tax-free when TRIS is in retirement phase.

TRIS turns into a regular retirement pension: A TRIS (Transition to Retirement Income Stream) converts into a regular retirement pension once you fully retire, turn 65, or meet any other condition of release. At that point, the withdrawal limits that applied to the TRIS are removed, and the account becomes a standard account-based pension.

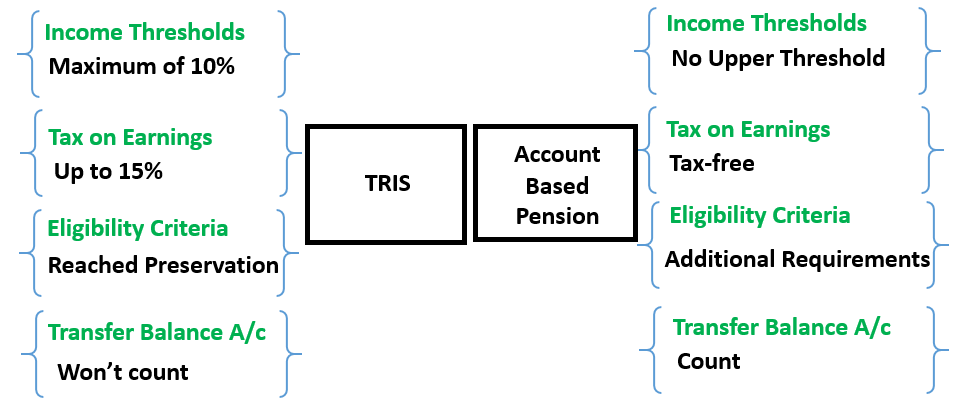

What is the difference between TRIS and Account Based Pension (ABP)?

Key change: From 1 July 2017, the tax and reporting rules for transition-to-retirement income streams (TRIS) were tightened. Before 1 July 2017, all TRIS payments were tax-exempt on investment earnings (known as exempt current pension income, ECPI). After 1 July 2017, only a TRIS in the retirement phase can get tax-exemption and count towards the member’s transfer balance cap of $2,000,000 for the financial year 2025-2026.

Retirement-phase TRIS: Earnings on the supporting assets are tax-exempt (ECPI), and the TRIS balance counts towards your transfer balance cap.

Non-retirement-phase TRIS:Earnings are taxed at normal rates (no ECPI benefit) and the TRIS balance does not count towards the transfer cap until it enters retirement phase.

When a TRIS Enters the “Retirement Phase”?

A TRIS automatically enters retirement phase only when the member meets a “condition of release” with nil cashing restrictions. These conditions are:

Age 65: Turning age 65 automatically puts a TRIS into retirement phase.

Retirement: For those aged 60+, “retirement” means leaving work with no intention to return (with trustee satisfaction). (If under 60 but at preservation age, retiring similarly triggers it.) In these cases, the member must notify their super fund to activate retirement phase.

Other conditions: Permanent incapacity or terminal illness also move the TRIS into retirement phase (again requiring fund notification).

A member does not need to commute or restart the TRIS to enter retirement phase. Once one of these conditions is met, the usual 10% annual withdrawal cap and commutation restrictions on TRIS payments are lifted once the TRIS is in retirement phase making it effectively the same as an ordinary account-based pension.

Join my webinar on 23th July- Accumlation to Pension: ABP, TRIS & other choices

Register now! Expand your knowledge! You are warmly invited to join my webinar and earn CPD hours!

❓Does a TRIS automatically convert to an account-based pension?

Answer: Yes

Yes, under Australian superannuation law, a TRIS will automatically convert to an account-based pension once the member satisfies a condition of release with a nil cashing restriction.

❓How do taxable and tax-free parts work?

Answer: When you move money from your super into a TRIS, the taxable and tax-free portions are automatically carried over in the same proportion from your existing super account.

You can’t choose how much of it is tax-free or taxable.

Let’s say your super account (before starting TRIS) looks like this:

Component

Amount

Proportion

Tax-free

$60,000

30%

Taxable

$140,000

70%

Total

$200,000

100%

If, you decide to move $100,000 into a TRIS.

👉 The tax-free and taxable portions of your TRIS will be:

· 30% of $100,000 = $30,000 tax-free

· 70% of $100,000 = $70,000 taxable

✅ Key Takeaways

TRIS is ideal for phased retirement or tax-effective income planning before full retirement.

It’s important to understand the cap limits, tax treatment, and conversion rules.

TRIS can still be a valuable part of a broader retirement strategy, especially when combined with salary sacrifice or personal contributions.

Visit www.trustdeed.com.au for more details or call us on(02) 9684 4199

.jpg)