💼 Contributions Over the Caps: What You Need to Know?

News | Mehak Gaba |Released: 31/07/2025 | Read: 5 Mins

There are annual limits, known as contribution caps, on how much you can contribute to your super. Exceeding these caps may result in additional tax liabilities.

Self-managed superannuation funds (SMSFs) offer flexibility for members to grow their retirement savings while accessing valuable tax concessions. Today, we outline the two main types of contributions: concessional (before-tax) and non-concessional (after-tax).

It is essential for accountants to understand the rules and implications of each contribution type to ensure compliance and help clients maximise their superannuation benefits.

In managing an SMSF, understanding the types of contributions is essential for tax planning, compliance, and maximising retirement savings. Broadly, contributions fall into two primary categories:

These are contributions for which a tax deduction is claimed either by the member or an employer. Concessional contributions are subject to 15% contributions tax upon entry into the SMSF.

Common types include(s):

Employer Super Guarantee (SG) contributions (currently 12% of ordinary time earnings).

Salary sacrifice contributions made under an agreement with the employer.

Personal contributions where the individual claims a tax deduction.

Transfers from reserves, where applicable

Note: From age 67 to 74, individuals must meet the work test to claim a personal deduction. This involves working at least 40 hours within a consecutive 30-day period in the financial year. This rule ensures super contributions are aligned with genuine retirement savings objectives.

✅Non-Concessional Contributions (After-tax):

Personal Contributions made into an SMSF from after tax income on which no tax deduction is claimed, and no entry tax applies.

Common types include(s):

Personal contributions not claimed as a tax deduction (generally any money on which you have already paid tax).

Eligible spouse contributions.

Contributions you make for a child under age 18.

Amounts transferred from a foreign super fund that do not count towards your Australian fund’s assessable income

You may come across other contribution types such as downsizer contributions, government co-contributions, or CGT-exempt contributions but in this newsletter, we have focused specifically on the two core categories: concessional and non-concessional contributions.

Note: From 1 July 2022, individuals aged67 to 74are no longer required to meet the work test to make non-concessional contributions.

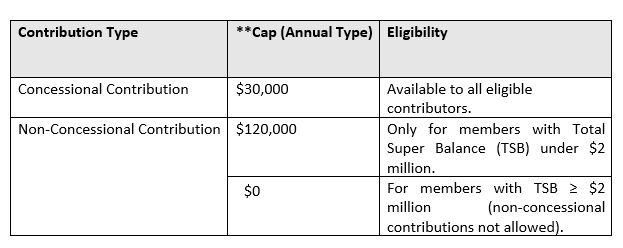

📈 2025/26 Annual Contribution Caps

🚨 Excess Concessional Contributions

If your concessional contributions exceed the $30,000 annual cap:

The excess is added to your assessable income and taxed at your marginal tax rate.

A 15% tax offset is applied to account for the tax already paid by your SMSF.

You are personally liable for the resulting tax and must pay it from your own funds.

It's essential to track all contributions across all super funds to avoid surprise tax bills.

Once your SMSF Annual Return is lodged, the ATO will issue a Determination and Notice of Assessment if you’ve exceeded the cap. You will need to decide how to manage the excess.

📝 Your Options

✅Option 1 Leave the excess concessional contributions in your SMSF

The excess concessional contributions will count toward your non-concessional contributions cap.

If your Total Super Balance is ≥ $2 million, this may cause you to breach your non-concessional cap, triggering further penalties.

This strategy is not available if you're already over the $2 million Transfer Balance Cap.

✅Option 2: Release up to 85% of the Excess from your SMSF

Amount: Up to 85% of excess concessional contributions may be released to help pay your personal tax.

Cap Impact: Released amounts do not count toward your non-concessional contributions cap.

How to Elect:

Submit an election via ATO Online Services or by completing the Excess Concessional Contributions Election Form.

Must be done within 60 days of the ATO's determination.

Important Notes:

Once submitted, the election is irrevocable.

The ATO will issue a Digital Release Authority via SuperStream—no funds should be released until this is received.

After receiving the authority, confirm your release request through your Client Portal Inbox.

Note: Caps apply per person, not per fund or employer.

🚨 Excess Non Concessional Contributions

It should be noted that there are Contributions Limits for Non-Concessional Contributions.

If you go over the Non Concessional Contributions cap ($120,000), the ATO will contact you by sending you a Determination letter after the lodgement of your SMSF Annual Return. You will be asked to choose how your Excess Non Concessional Contributions are taxed. You have the following options:

📝 Your Options

✅ Option 1: Release the Excess Non-Concessional Contribution

If you exceed the non-concessional cap, you may elect to release the excess amount along with associated earnings from your superannuation fund.

The earnings component will be included in your personal assessable income and taxed at your marginal tax rate.

A 15% non-refundable tax offset is available to reduce the tax payable on these earnings.

This option avoids the 47% excess contributions tax that would otherwise apply to the excess amount.

You must make this election within 60 days of the ATO’s determination, either via ATO Online Services or using a paper election form.

No funds may be released until the ATO issues a Digital Release Authority to your SMSF via SuperStream.

Once the authority is received, your SMSF administrator can proceed with the release of the amount.

⚠️ Releasing the excess is generally the more tax-effective option.

❌ Option 2: Leave the Excess in Super and Pay the Tax

If you choose not to release the excess contribution:

The entire excess non-concessional amount will be taxed at the highest marginal tax rate (currently 47%).

You will not be able to later reverse or withdraw the excess to mitigate this tax.

As this tax applies to after-tax contributions, the effective tax impact may exceed 90%, making this a very costly option.

This approach is generally not recommended unless there is a strategic reason to retain the excess in super despite the penalty.

By understanding and applying these rules, accountants can help their SMSF clients make informed contribution decisions, maximize tax concessions, and keep their retirement savings on track.

⚖️ Carry-Forward of Unused Concessional Contributions

Under Section 292-85(6) of the Income Tax Assessment Act 1997 (Cth), from 1 July 2018, eligible individuals are permitted to make carry-forward concessional contributions, provided they meet certain conditions.

To qualify:

The member’s Total Superannuation Balance (TSB) must be less than $500,000 on 30 June of the previous financial year; and

The member must have unused concessional contribution cap amounts from one or more of the previous five financial years.

Key Points:

Any unused concessional cap amount that is not used within five years will expire.

The first year from which unused concessional contributions could be applied was the 2019–20 financial year (i.e. based on unused amounts from 2018–19 onwards).

Including carry-forward provisions in your trust deed is essential for ensuring compliance and contribution flexibility. Our trust deed includes these provisions under Clause 60, allowing members to carry forward unused concessional contributions. If your current deed does not contain this feature, we can assist you in updating your super fund deed accordingly

⚖️ Join our webinar on 4th September, 2025- Maximise Your Super: Understanding Contributions

.jpg)