Division 293 tax on concessional contributions by high-income earners

News | Mehak Gaba |Released: 13/08/2025 | Read: 5 Mins

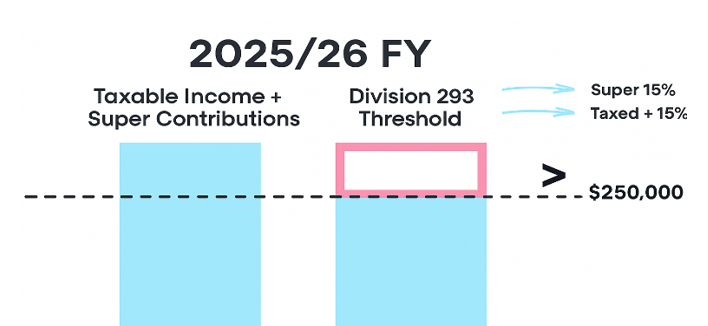

Division 293 tax is an additional 15% tax for individuals whose taxable income and concessional contributions combined exceed $250,000 threshold in a financial year. This means the tax rate on the portion above the $250,000 threshold increases from 15% to 30%.

Even though you may pay tax at a rate of 30% on all or part of your concessional contributions, this is still significantly lower than the top marginal tax rate of 47% (including the Medicare levy) that high-income earners face.

For those earning above or nearing the $250,000 threshold, it is important to understand how this Division 293 tax operates?

What counts as " Taxable Income" Under Division 293?

The income component of the Division 293 tax calculation is based on the same methodology used for the Medicare Levy Surcharge (MLS), but excludes reportable superannuation contributions.

It is calculated by:

Adding:

Taxable income (assessable income minus allowable deductions)

Total reportable fringe benefits amounts

Net financial investment loss

Net rental property loss

Net amount on which family trust distribution tax has been paid

Subtracting:

Super lump sum taxed elements with a zero tax rate

Assessable first home super saver released amount

The result is your Division 293 income.

What counts as " Super Contributions " under Division 293?

Important Points:

Only Concessional contribution: $30,000 per person.

SG rate: Employers must contribute 12% of your ordinary time earnings (counts towards the cap).

Carry-forward rule: Under Section 292-85(6) of the Income Tax Assessment Act 1997 (Cth), if your total super balance is under $500,000 at the previous 30 June, you can use up to 5 years of unused cap amounts.

Expiry: Unused amounts expire after 5 years, starting with the oldest first.

Tax treatment: Contributions are generally taxed at 15% inside super (plus extra 15% Division 293 tax for high-income earners).

Example – Using Carry-Forward Concessional Contributions

Total super balance at 30 June 2025: $420,000 (✅ under $500,000, so eligible)

Unused cap amounts from previous years:

2020–21: $7,500 unused

2021–22: $10,000 unused

2022–23: $5,000 unused

2023–24: $2,000 unused

2024–25: $8,000 unused

Total unused cap available in 2025–26: $32,500 ($7,500 + $10,000 + $5,000 + $2,000 + $8,000)

In 2025–26, you can contribute:

Normal cap: $30,000

Plus carry-forward unused cap: $32,500

Total possible concessional contributions:$62,500 (before triggering excess contributions rules).

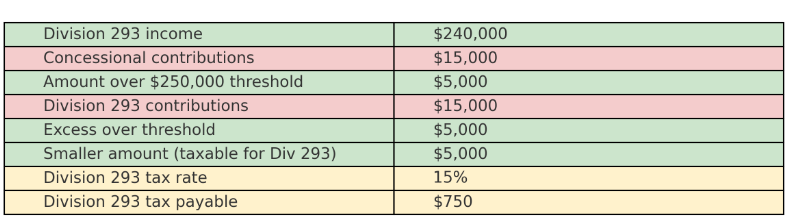

Division 293 tax calculation

How do I know if I have to pay Div 293 tax and what do I need to do?

The ATO will work out if you need to pay Div 293 tax based on information in your tax return and data they receive from your super fund(s).They will issue you with a notice of assessment stating the amount of tax payable.

There are two options for paying:

(a) With your own money: Use personal funds and pay the ATO directly.

(b) Releasing money from super: If you get a Division 293 tax bill, you can choose to pay it using money from your superannuation.

How it works:

Complete a Division 293 election form to authorise the ATO to take the payment from your super.

You have 60 days from the date on your Division 293 Notice of Assessment to lodge this form.

This 60-day period is only to make your decision.

It does not extend the payment due date on your notice — your tax must still be paid on time.

The fastest way to lodge is online, which sends your form straight to the ATO.

What happens next:

Once the ATO receives your valid election, they will send a release authority to your nominated super fund(s).

Your fund will send the nominated amount to the ATO.

The ATO will use this money to pay your Division 293 tax. If there’s any leftover, it will go towards other tax or government debts first, then any remaining balance will be refunded to you.

Important: Once you make an election, you cannot cancel or change it.

⚖️ Join our webinar on 4th September, 2025- Maximise Your Super: Understanding Contributions & Division 293

Division 293 tax can apply even if an individual’s income is normally below $250,000. Certain one-off events may push total income over the threshold in a particular year, triggering the additional tax. Examples include:

Receiving an eligible termination payment

Realising a capital gain

Any other significant, one-off increase in income

How to reduce the Division Tax Burden?

Prioritise Non-Concessional Contributions: Non-concessional contributions (made from after-tax income) aren’t subject to Division 293 tax. When appropriate, members should consider prioritizing these contributions over concessional contributions to avoid the additional tax.

Limit Salary Sacrifice Contributions: Review and adjust salary sacrifice plans regularly. If a member is nearing the $250,000 threshold, consider reducing or halting salary sacrifice, especially during high-income years, to avoid triggering Division 293.

Manage Capital Gain: Spreading capital gains across multiple years or timing the sale of assets more strategically can help manage income spikes that could push the member’s income over the Division 293 threshold.

Monitor Unused Concessional Caps: The carry-forward concessional contributions strategy can be beneficial, but using unused caps without considering income projections can lead to unexpected Division 293 tax liabilities. It’s essential to plan carefully.

Time Contributions Strategically: If a client expects a significant income boost (e.g., property sale, redundancy, or investment gain), it may be wise to defer concessional contributions to a year with lower income. This reduces the likelihood of surpassing the $250,000 threshold

Visit www.trustdeed.com.au for more details or call us on(02) 9684 4199