Work Test Exemption: One-Time Opportunity to Contribute After Retirement

News | Mehak Gaba |Released: 10/09/2025 | Read: 5 Mins

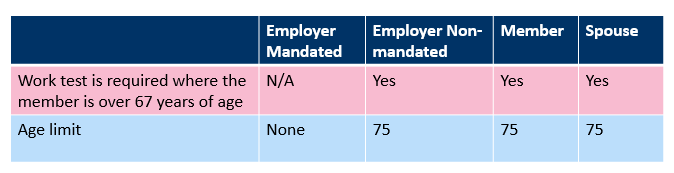

In Australia, the superannuation work test applies to individuals aged 67–74 who wish to make voluntary contributions (such as Non concessional contributions or salary sacrificed contribution) to their super.

To meet the test, you must be *gainfully employed for at least 40 hours within a consecutive 30-day period during the financial year in which the contribution is made.

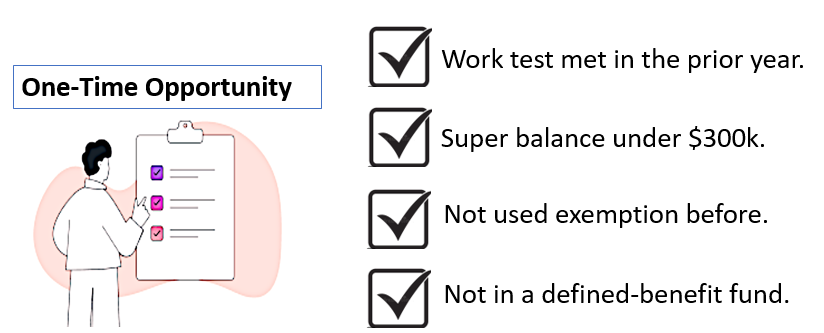

Even, If you don’t meet the work test this year, you may still be able to contribute by using the work test exemption, as long as you meet the following conditions:

You satisfied the work test (40 hours within a consecutive 30-day period) in the previous financial year;

Your total super balance was less than $300,000 at the end of the previous financial year; and

You have not previously used the exemption.

You are not a member of a defined benefit fund.

Under this exemption, your super fund can accept voluntary contributions for up to 12 months after you last met the work test, even if you are no longer working.

What is "Gainfully Employed" ?

The Superannuation Industry (Supervision) Regulations 1994 defines gainfully employed as "employed or self employed for gain or reward in any business, trade, profession & occupation or employment and does not include voluntary or unpaid work.

To be considered gainfully employed, a person must provide a service and be remunerated for it. The ATO has provided the following information on what gainfully employed means - "Gain" or "reward" is the receipt of remuneration such as wages, business income, bonuses and Commissions.

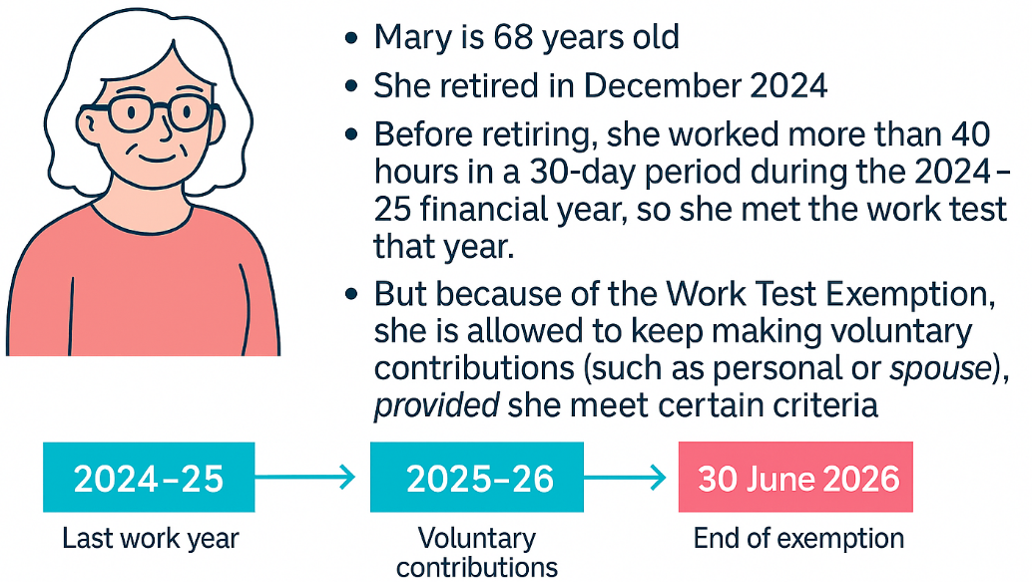

Work Test Exemption: Practical Example 1 of 3

Explanation:

👉 Normally, after retiring, she wouldn’t be able to contribute in the next financial year unless she met the Work Test last financial year.

👉Under the Work Test Exemption, she is allowed to continue making voluntary contributions (such as personal or spouse contributions) for one additional financial year (2025–26) — even though she is no longer working.

👉 In short: Mary’s last work year was 2024–25. Thanks to the exemption, she can still contribute until 30 June 2026.

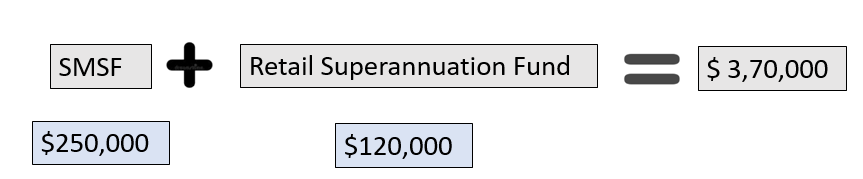

Work Test Exemption (Incorrect Contributions) : Practical Example 2 of 3

Explanation:

Sally, aged 68 met the gainful employment test during 2024/25 prior to retiring in May 2025.

She had a balance in her SMSF of $250,000 so she made a non-concessional contributions of $100,000 in August 2025.

In addition to her SMSF sally had a retail superannuation fund with a balance of $120,000 meaning her total superannuation balance at 30th June 2025 was $3,70,000.

👉 Sally was ineligible to make a work test exemption contribution so the $100,000 needs to be returned by the trustees.

Work Test Exemption (Not Gainfully Employed) : Practical Example 3 of 3

Explanation:

Mary (67 years old)

Mary volunteers at her local animal shelter and retired in F.Y 2024-2025.

She spends 50 hours in July helping them with admin and animal care.

She does not receive any payment, only reimbursement for petrol.

➡ This does NOT count as gainful employment (unpaid voluntary work).

❌ Mary cannot claim the Work Test Exemption in F.Y 2025–26.

⚖️ Join our webinar on 18th September, 2025- Maximise Your Super: Understanding Contributions & Division 293

It should be noted that all contributions that are not mandated employer contributions or downsizer contributions must be made within 28 days following the month an individual turns 75.

A work test decleration should be signed each financial year in which contributions are made after turning 67. SMSF Trustees are responsible for ensuring that members have met the requirenments prior to making contributions & evidence should be retained to substantiate for audit purpose.

If non working member makes a contribution post 67, and they did not satisfy the criteria for the work test exemption- the trustees are unable to accept the contribution. If a contribution is inadvertently made it must be returned within 30 days.

If a member who qualifies for the work test exemption makes a contribution that exceeds their non concessional cap then the trustees cannot return the excess amount and the member will be assessed for excess non-concessional contribution.

Visit www.trustdeed.com.au for more details or call us on(02) 9684 4199