What an SMSF should do after paying out an LRBA Loan?

News | Mehak Gaba |Released: 15/10/2025 | Read: 5 Mins

Once the borrowing under a Limited Recourse Borrowing Arrangement (LRBA) is paid back, the SMSF trustee has two options:

It can retain the property in the bare trust, or

It can transfer title to the property from the bare trust to the SMSF trustee.

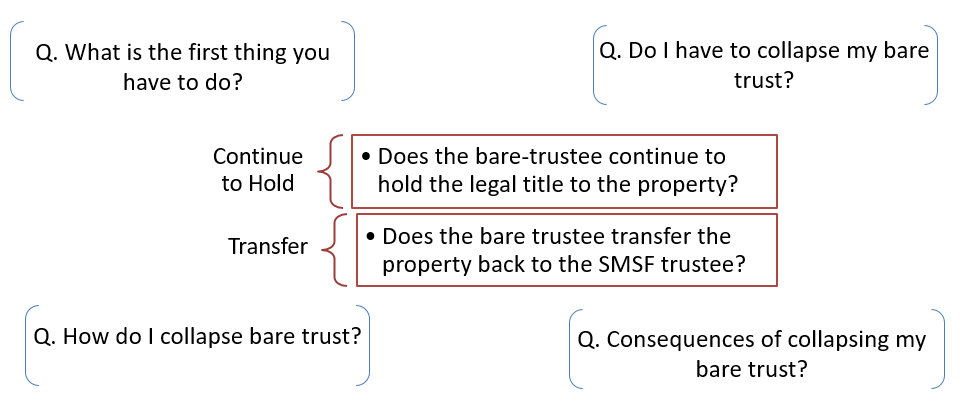

What is the first thing you have to do?- Debt mortgage formally released.

Do I have to collapse my Bare Trust Deed?- It depends from case to case.

How do I collapse my Bare Trust Deed?- Bare trustee transfers the property down to the SMSF Trustee.

Consequences of collapsing Bare Trust Deed?-

Duty rules vary between states, so the implications differ depending on the jurisdiction.

It is important to ensure the bare trust is a complying arrangement; otherwise, the SMSF may be liable for double duty.

Can an asset be left in a Bare/Holding Trust? -SPR 2014/1 & S71(8) of SIS Act, 1993

Background

The SMSF trustee’s interest is in the bare/holding trust, which could be considered a "Related Trust."Under SIS rules, an investment in a related trust is generally treated as an in-house asset, and SMSFs are typically restricted from holding more than 5% of their assets in such investments.

To address this concern, the legislature introduced an exception to the in-house asset rules. Section 71(8) of the Superannuation Industry (Supervision) Act 1993 (Cth) provides that an investment in a related trust, made solely to satisfy the requirements of an LRBA, is excluded from being treated as an in-house asset and the property can continue to hold in Bare Trust Deed. This allows the property to continue being held under a bare trust deed without breaching the in-house asset rules.

Purpose of the Ruling (ATO SPR 2014/1)

This ruling clarifies the circumstances in which an asset held by a related trust under an LRBA is not treated as an in-house asset of an SMSF. It also confirms that the asset may continue to be held in the related (bare/holding) trust even after the LRBA has been fully repaid.

Prevents Technical Breaches:

The ruling ensures that timing differences between the loan repayment and asset acquisition do not inadvertently cause the asset to be classified as an in-house asset, thereby preventing technical breaches of the SIS Act.

Retrospective Application:

The determination applies retrospectively from 24 September 2007, although it was issued in April 2014.

If an Asset is left in Bare/Holding Trust, Can it be replaced?

One of the key requirements of LRBAs is that the asset being acquired cannot be replaced during the life of the loan.

If the asset is subdivided or otherwise fundamentally altered, the ATO considers this to constitute a replacement (see SMSF Ruling SMSFR 2012/1). Accordingly, SMSF trustees who wish to significantly improve or alter assets acquired through an LRBA must first transfer the title to an SMSF. For s 71(8) to apply, the asset must not have been replaced.

Therefore, under a strict interpretation of the proposed law, an asset left in a bare/holding trust cannot be fundamentally altered (i.e., “replaced”), even after the loan is repaid.

It is hoped that a practical approach will be adopted in due course, but the conservative approach for now is to assume that fundamental alterations are not permitted.

When the asset held by a bare trust is real property, the transfer of legal title to the SMSF generally involves the following steps:

Confirm Loan Re-payment:Obtain written confirmation from the lender (bank or related party) that:

(a) The LRBA loan is fully repaid, and

(b) Any mortgage has been discharged and keep this as evidence for Revenue NSW.

Legal Documentation: Engage a solicitor to prepare the necessary resolutions between the trustee of the bare trust and the trustee of the SMSF.

Transfer Preparation: The solicitor will also prepare the transfer documents in accordance with the requirements of the relevant state or territory land titles office.

Stamping Requirements: Arrange for the transfer documents to be stamped. Depending on the jurisdiction, additional supporting documents may be required to apply for a stamp duty exemption or concession. Attach Supporting documents:

(a) Copy of stamped bare trust deed.

(b) Copy of SMSF deed.

(c) Discharge of mortgage (proof loan repaid).

(d) Declaration / statutory declaration confirming no change in beneficial ownership.

VIC: No Duty is chargeable on transfer (Section 41 of Duties Act, 2000).

Other States/Territories: Please check with the revenue department of State.

5. Registration: Once stamped, lodge the transfer for registration with the relevant land titles office.

To qualify for a stamp duty exemption or concession, it must be demonstrated that the bare trust arrangement was properly established and duly stamped at the outset, and that the SMSF provided all of the purchase money for the asset.

Important Points to note down:

1. Transferring Title from a Bare Trust to the SMSF enables Property Modifications Post-Payment: Transferring title from a bare trust to the SMSF allows the fund to modify the property (e.g., subdivide a single title) once the debt is repaid—changes are not permitted while the property remains in the bare trust.

2. Bare Trust Cannot Be Reused even if title is transferred: A new bare trust arrangement is required for any new LRBA property purchases but the same company can act as trustee for the new bare trust.

3. Retain all LRBA documentation for as long as the asset remains in the holding or bare trust: It is essential for SMSF trustees to retain all LRBA documentation for as long as the asset remains in the holding or bare trust. Auditors will typically request the holding/bare trust deed and the original loan agreement to verify that the LRBA was compliant and that the fund continues to meet the in-house asset exemption requirements.

4. Deregister the Trustee Company: Once the LRBA is fully repaid and the legal title to the property is transferred from the bare trust to the SMSF, the bare trust is no longer needed.Consequently, the corporate trustee of the bare trust can be deregistered.

How can Trustdeed help?

For assistance with preparing a bare trust deed & stamping, please contact us on 02 9684 4199.

Get everything done in one place – we set up your bare trust deed and handle the stamping for you too. Fast, simple, and hassle-free! Stamping available for

NSW ($440) + Govt fees ($750)

Victoria ($132)

Set up Bare Trust deed cost you $330.

Visit www.trustdeed.com.au for more details or call us on(02) 9684 4199