News | Mehak Gaba |Released: 09/10/2025 | Read: 5 Mins

Under subsection 67A(1) of the Superannuation Industry (Supervision) Act 1993 (SIS Act), the trustee of a regulated superannuation fund (such as an SMSF) may enter into a Limited Recourse Borrowing Arrangement (LRBA) to acquire a single acquirable asset.

This rule applies to all LRBAs established on or after 7 July 2010.

Meaning of “Acquirable Asset”

The term “acquirable asset” is defined in section 67A(2) as:

“An asset which is not money (whether Australian currency or currency of another country), and which the trustee is not prohibited by the SIS Act or any other law from acquiring.”

The word “asset” itself (per subsection 10(1) of the SIS Act) means:

“Any form of property.”

Hence, an acquirable asset can be any property (e.g., land, shares, units, or equipment) that the fund is legally permitted to acquire, other than money.

Meaning of “Single Acquirable Asset”

Although “Single acquirable asset” is not defined in the Act, the ATO has clarified its meaning through SMSFR 2012/1.

According to the ruling:

A Single acquirable asset is one identifiable asset (or a collection of assets) that are inseparable — that is, they must be dealt with together under law or by their nature.

If a law, contract, or physical characteristic requires multiple components to be sold or transferred together, they are treated as one asset for LRBA purposes.

However:

If the components can be sold or dealt with separately, they are not a single acquirable asset.

Separate LRBAs would be required for each one.

Join my webinar on 16th October, 2025

ATO SMSFR 2012/1: Main Focus Areas

In May 2012 the ATO released SMSF Ruling SMSFR 2012/1 to clarify key concepts for limited recourse borrowing arrangements (LRBAs). The ruling confirms that an SMSF may borrow only to acquire a single acquirable asset held in a separate holding trust, and it outlines the narrow circumstances under section 67B in which the asset may be replaced without invalidating the LRBA.

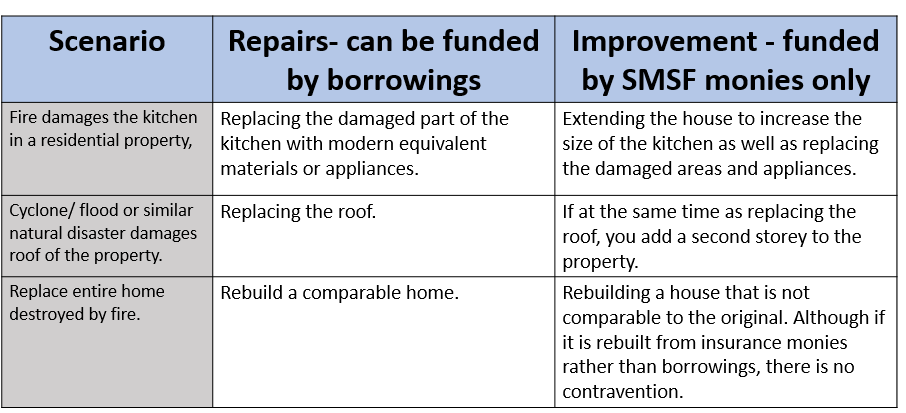

It also clarifies that borrowed funds can cover acquisition costs and permissible repairs or maintenance, but improvements to the asset cannot be financed by the LRBA.

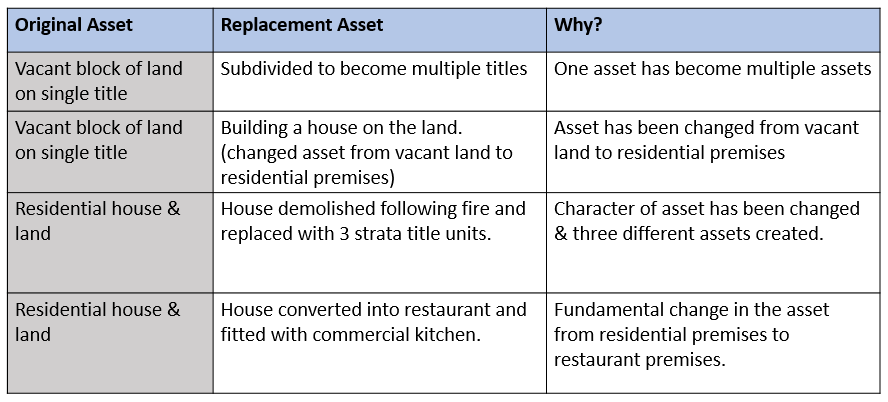

Single Acquirable Asset: An LRBA can involve only one asset or object of property. SMSFR 2012/1 emphasizes that both the legal title(s) and the physical substance of the asset must be considered. If parts of a proposed purchase (for example, separate titles or detachable fixtures) can be dealt with separately, they constitute multiple assets. Conversely, if legal form or contractual restrictions require components to transfer together, they count as one asset.

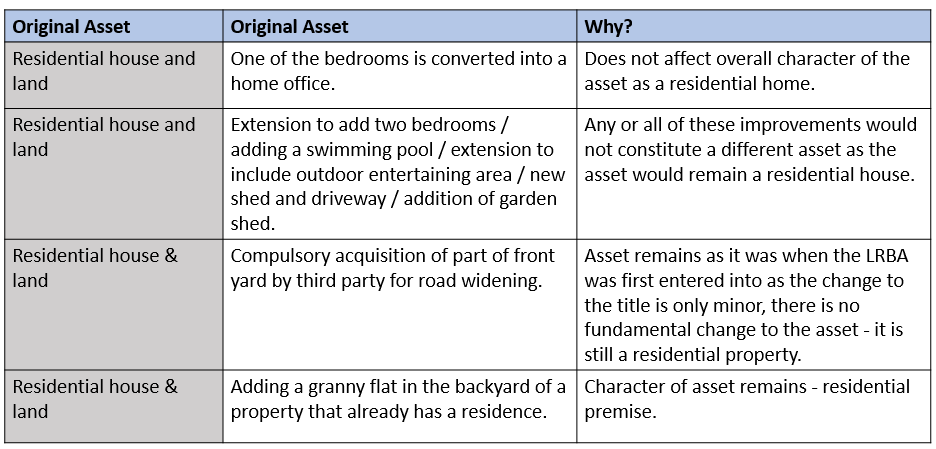

Replacement Asset (S67B): Section 67B of the SIS Act permits the LRBA to continue when the original asset is replaced by another of the same kind in very limited situations. For example: One of the bedrooms is converted into a home office. Outside those exceptions, replacing the asset breaks the LRBA. For example, if an item of equipment is destroyed and replaced by the insurer, the replacement asset is not covered by S67B and the LRBA fails.

Repairs vs. Improvements: Borrowed money under an LRBA may fund maintenance or repairs of the acquirable asset (keeping it in its original state). However, an improvement – a substantial upgrade or addition that significantly increases the asset’s value or functionality – cannot be paid for with LRBA funds. Improvements must be financed from SMSF funds,and must comply with SMSF rules not LRBA borrowing, and must comply with SMSF rules.

LRBA Structure: All requirements of SISA section 67A must be met. The asset must be held in a separate bare (holding) trust for the SMSF, with the SMSF trustee holding beneficial title and the lender’s security limited to that asset. The loan documentation should clearly apply only to that single acquirable asset (purchase price, related fees and permitted repairs) to maintain compliance.

Official ATO Examples

Apartment + Car Park: An SMSF acquires a strata apartment and a separately titled car park. A restriction on title transfers means the titles must transfer together. The ATO treats the apartment and car park as one single acquirable asset, so one LRBA can cover both.

Land & House Purchase: In Example 9, the SMSF buys vacant land and then uses borrowed funds to build a house. Using loan funds to construct the house upgrades the asset (from “vacant land” to “residential land”), breaching the LRBA conditions. In Example 10, the SMSF contracts to buy the land together with a house to be built (settlement after construction). In that case, the land+house is treated as one asset from the outset, and a single LRBA can fund it.

Cattle Farm Expansion: An SMSF buys a 10,000-hectare cattle property under an LRBA. It then uses SMSF cash to build a large cattle shed. The shed is an improvement, but it does not change the property’s fundamental character (it’s still a cattle farm). The ATO confirms the LRBA remains valid in this case.

Farm + Residence Addition: An SMSF buys a one-hectare hobby farm under an LRBA and then builds a house on it for on-site living. Adding the house does change the asset’s character (from a farm to a farm-plus-residence). The ATO treats this as creating a different acquirable asset, illustrating how certain improvements can effectively yield a new asset.

The examples above illustrate how SMSFR 2012/1 applies in practice. Trustees should structure each LRBA exactly according to the rules.

In summary: ensure only one asset is acquired per loan, use the borrowed funds only for that asset (purchase costs and permitted repairs), and avoid using loan proceeds to make substantial improvements or buy an another asset. By following these principles – and referring to SMSFR 2012/1’s detailed examples – SMSF trustees, accountants and financial advisers can confidently comply with the LRBA requirements and avoid unintended breaches

How can Trustdeed help?

For assistance with preparing a single contract for your SMSF property, please contact us on 02 9684 4199.

Get everything done in one place – we set up your bare trust deed and handle the stamping for you too. Fast, simple, and hassle-free! Stamping available in

NSW ($440) + Govt fees ($750)

Victoria ($132)

Visit www.trustdeed.com.au for more details or call us on(02) 9684 4199