News | Mehak Gaba |Released: 18/09/2025 | Read: 5 Mins

An in-specie transfer (also known as an in-specie contribution) occurs when an asset is transferred directly into an SMSF rather than being sold and contributed as cash.

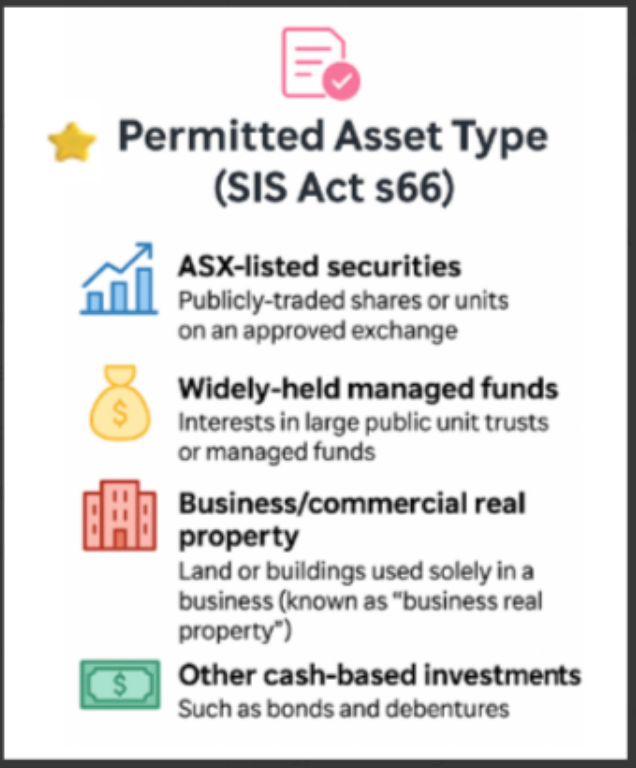

Under section 66 of the SIS Act, SMSF trustees are generally prohibited from acquiring assets from a related party. However, certain categories of assets—referred to as “permitted assets”—are specifically allowed to be transferred in this way.

The only assets currently allowed to be transferred to an SMSF from a Member (or an associate of an SMSF Member by blood or marriage or entity controlled by a Member) are as follows:

ASX Listed Securities

Widely Held Managed Funds

Business or Commercial Property

Cash Based investments such as Bonds and Debentures.

An SMSF cannot purchase Residential Property from a Member (or an associate of a Member including family members by blood or marriage or entities controlled by the Member) even if the purchase is at market value.

SMSFR2009/1: Example 14- often called the "Woods case"

Explanation:

Mr. Woods owned a number of residential properties–20 in total. Some of those properties were already inside his super fund, and some were held outside. Now, Woods wanted to transfer one of those blocks of flats into his SMSF as an in-specie contribution.

Now, normally, we think ofbusiness real propertyas warehouses, factories, or offices– but in this ruling, the ATO looked at whether hisresidential propertiescould qualify. The key was that Woods wasn’t just a passive investor. He was actively managing those properties himself – collecting rent, handling tenants, taking care of the day-to-day running.

And that’s where the ATO set out two important criteria:

Number of properties–it wasn’t just one or two, it was a larger portfolio.

The level of personal involvement–Woods wasn’t outsourcing this to a real estate agent; he was running it as his business.

So, in short – even though they were residential properties but managing them wasWoods’ business,

Hence, they were treated asbusiness real property. And that meant he could transfer one of those properties in specie into his SMSF instead of cash.

Key Elements: In-Specie Transfers

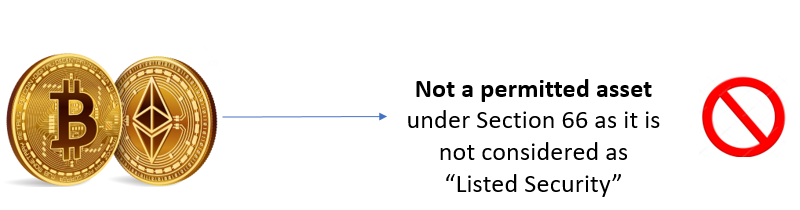

Can you make an in specie transfer of a personally owned crypto holding into an SMSF?

Explanation:

The answer is No. Under superannuation law, an SMSF can only acquire certain types of assets from a member or a related party — primarily business real property, listed securities, and certain in-house assets permitted under the legislation.

Cryptocurrency does not fall within these exemptions. While it is often referred to as a form of currency, the ATO does not treat crypto as cash or as an eligible asset class for in-specie transfer into an SMSF.

Although this position may change in the future, as of now an SMSF cannot acquire a personally held cryptocurrency holding from a member.

Potential Issues: In-Specie Contribution

Key Considerations Before Making an In-Specie Contribution

Access Restrictions: Once assets are transferred into superannuation, they are preserved and cannot be accessed until you reach your preservation age (or meet another condition of release).

Stamp Duty: Certain transfers—such as commercial property—may attract stamp duty. Always confirm the implications with the State Revenue Office or your solicitor.

Capital Gains Tax (CGT): Transferring assets into an SMSF changes ownership and may trigger CGT. While superannuation is generally a tax-effective environment, a significant capital gain may outweigh the benefits of contributing in-specie. The existence of the option does not necessarily mean it is the best choice for your situation.

Record Keeping: Accurate and comprehensive documentation of all transactions is essential to ensure compliance and to meet audit requirements.

In-specie contributions can be an effective way to transfer existing investments into the tax-advantaged superannuation environment. However, they involve complex rules and potential tax consequences. It is vital to seek professional advice before proceeding with any transaction.

Visit www.trustdeed.com.au for more details or call us on(02) 9684 4199