Division 293 vs Division 296: Key Similarities and Differences

News | Mehak Gaba |Released: 26/11/2025 | Read: 5 Mins

If you ever received unexpected tax bill from ATO and had no idea where it came from, chances are you have met Division 293 Tax. It is a rule that catches many high income earners mainly because it is not something that your employer considers in PAYG withholding, and it usually does not appear on the radar until the ATO comes knocking by notice of assessment or when you lodges your tax return at the end of the financial year.

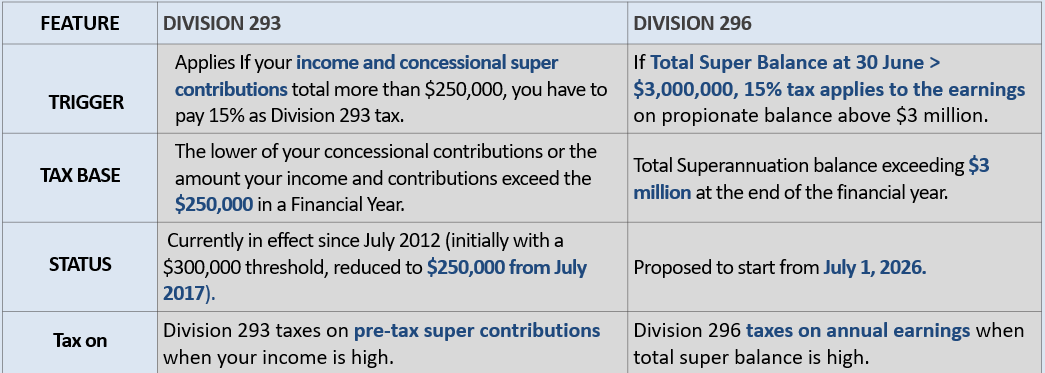

Division 293 Tax is an additional 15% tax on certain super contributions on high income earners. It applies when your income plus concessional contributions exceeds $250,000. That's on the top of 15% already applied in super.

Now, let's move to proposedDivision 296 Tax, it is also an additional 15% tax on high income earners whose total super balance exceeds $3 million as at 30 June each year. It applies only to the portion of earnings related to the balance above $3 million.

How They Differ?

Similarities Between Division 293 and Division 296 (Proposed)

Both are personal taxes — the tax is assessed to the individual member, not the SMSF or the super fund.

Division 293 and Division 296 do not tax the super fund itself. Instead, the ATO calculates the tax for each member personally. The tax notice is issued directly to the individual, even though it relates to their superannuation activity. The member can choose to:

2. Both apply an additional 15% tax once their respective thresholds are triggered.

In both cases, the extra 15% is in addition to existing superannuation tax rates, narrowing the tax advantage available to higher-income or high-balance individuals.

3. Both are designed to reduce superannuation tax concessions for higher-income or higher-balance individuals. The purpose of both laws is policy-driven:

In short, both measures target equity within the super system by limiting excessive tax concessions.

4. Both are administered by the ATO and issued as a personal tax assessment (similar to a tax bill). The ATO automatically:

Pay the tax personally, or

Elect to release money from their super fund to pay it. This reinforces that the liability belongs to the person, not the SMSF.

Division 293 adds an extra 15% tax on concessional contributions when income + contributions exceed $250,000.

Division 296 adds an extra 15% tax on super earnings when the total super balance exceeds $3 million at 30 June.

High-income earners receive the largest dollar benefit from concessional contributions (15% tax vs much higher marginal tax rates), so Division 293 reduces this advantage.

Individuals with very large super balances accumulate disproportionately large tax-free earnings due to the concessional tax environment, so Division 296 aims to moderate those benefits.

Collects required information from super funds and employers

Calculates the relevant tax

Issues a “Notice of Assessment” to the individual This notice works the same way as a normal tax bill, with payment options and due dates. The individual can again choose to release money from super to pay the assessment.

Division 293 and Division 296 both aim to make the superannuation system fairer by reducing the level of tax concessions available to higher-income or higher-balance individuals. Division 293 already applies to high-income earners, adding an extra 15% tax on concessional contributions once the $250,000 threshold is exceeded.

Division 296, however, is still a proposal and not yet finalised. If implemented from 1 July 2026, it will impose an additional 15% tax on earnings linked to super balances above $3 million.

Importantly, both taxes are assessed directly to the individual member, not the SMSF or the super fund, and are issued by the ATO as a personal tax assessment. Together, these measures are intended to support a more equitable and sustainable superannuation system—though Division 296 is still subject to legislative approval before it becomes law.

Visit www.trustdeed.com.au for more details or call us on(02) 9684 4199

.png)