Super Strategy for Australian Couples: Spouse Splitting

News | Mehak Gaba |Released: 20/11/2025 | Read: 5 Mins

Most people have never heard of this strategy, yet it can help you retire earlier, reduce tax, and even increase your Age Pension entitlements. The best part? You don’t need to contribute more — it’s simply about being smarter with what you already have.

In this session, I will explain how contribution splitting works and why it is a genuine game-changer. Once you understand it, it can completely reshape how you think about super.

Let’s begin with what contribution splitting actually is. It is a strategy that allows you to transfer a portion of your concessional contributions into your spouse’s superannuation account.

Only concessional contributions are eligible to be split. These include:

Superannuation Guarantee (employer) contributions

Salary sacrifice contributions

Personal deductible contributions for which you claim a tax deduction

You can split up to 85% of these contributions.

For this strategy, the definition of spouse includes a person of any gender who meets the eligibility criteria under superannuation law as discussed above.

It’s also important to remember that contribution splitting is different from making contributions directly to your spouse’s super. Instead, it involves transferring part of the contributions already made into your super account over to your spouse’s super account.

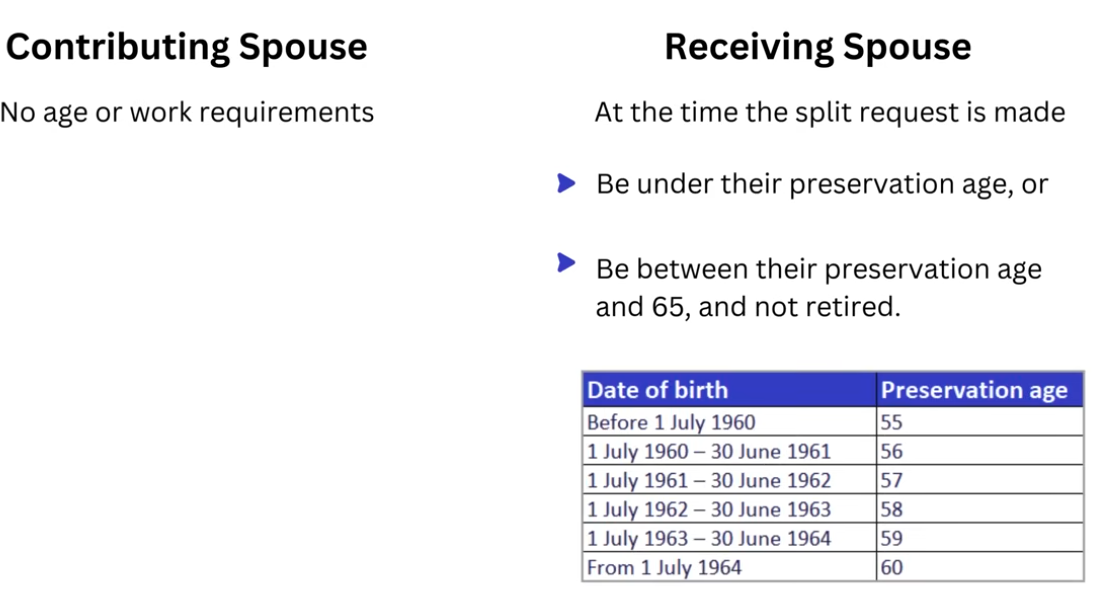

Who is eligible?

To use this strategy there is no age or work requirenments for the contributing spouse. However, at the time the spilt request is made the receiving spouse must meet the conditions specified in Sub regulations 6.44 (2) (c) of SIS Act. The below conditions are:

Age Restriction on receiving Spouse: The receiving spouse must not be 65 years or older at the time of application. Alternatively, if they are between their preservation age and 65 years, then the application will only be valid if they have not satisfied a condition of release.

Declaration from the Spouse: If the spouse is aged between their preservation age and 65, they need to give a statement at the time of application that they do not satisfy the relevant “condition of release.

Important Note: You can't apply to split your contributions if your spouse is aged 65 or over.

When you can apply?

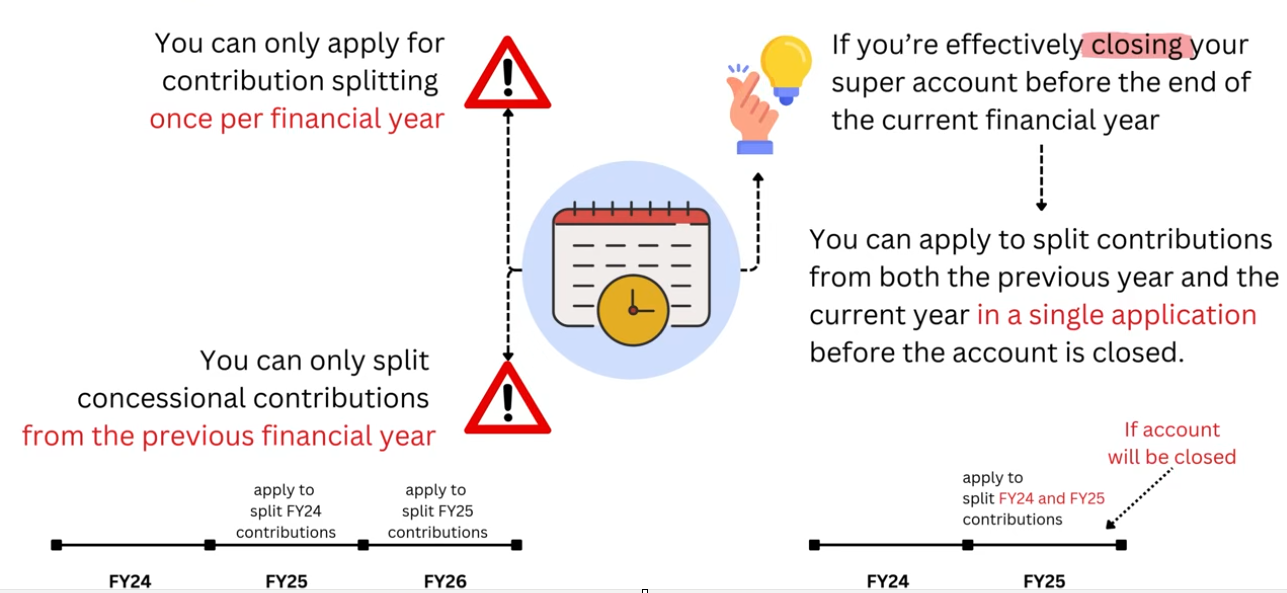

There are two key rules and one important exception:

You can apply for contribution splitting only once per financial year.

You can only split concessional contributions from the previous financial year.

For example, if you are applying in FY 2025, you can only split concessional contributions made in FY 2024, not from any earlier years.

To split your FY 2025 contributions, you must wait and apply in FY 2026.

The above is the standard process.

The exception is when you are planning to close your super account before the end of the current financial year. In that case, you may apply to split contributions from both the previous financial year and the current financial year in a single application, provided the application is lodged before the account is closed.

Practical Case Study

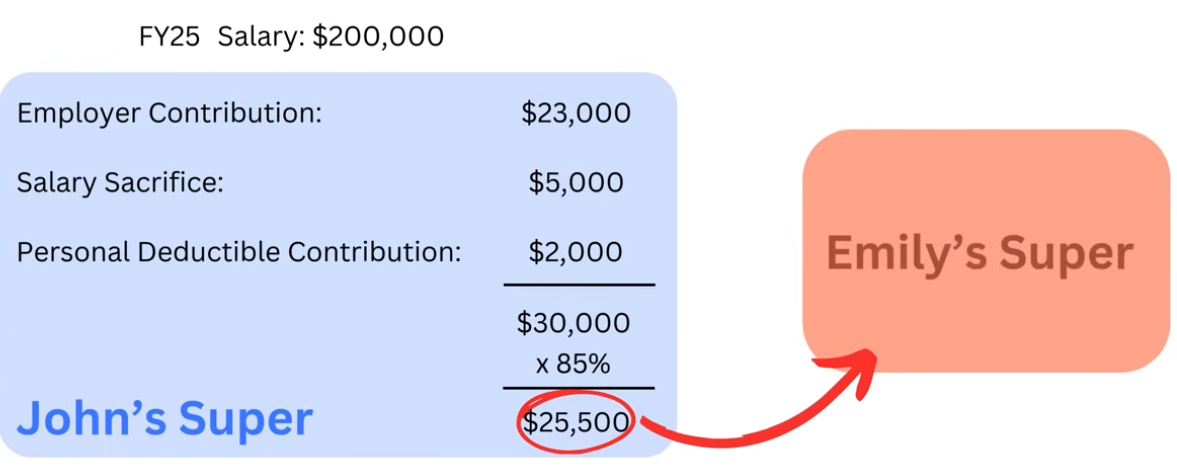

Let’s consider an example involving a couple, John and Emily.

In the 2025 financial year, John earned $200,000. His employer contributed $23,000 to his superannuation, he salary sacrificed an additional $5,000, and he made a personal deductible contribution of $2,000. This brings his total concessional contributions to $30,000.

John can choose to split up to 85% of these contributions — that is, $25,500 — into Emily’s superannuation account.

Check if the super fund trust deed allows spouse splitting.

Use the official ATO form NAT15237 (Superannuation contributions splitting application).

Provide both your spouse and your spouse's personal and super account details, and specify the amount you want to split.

The Trustee must process any application to split a contribution within 90 days of receiving the application from a member.

Invalid applications

Your application to split your contributions is invalid if any of the following apply:

you have already applied in that financial year and the trustee of your fund has received your application.

the amount of benefits you have applied to split is more than the maximum amount that can be split.

your spouse is 65 years and over.

your spouse has reached their preservation age and is retired.

Conclusion: The Real Benefits

Earlier Access to Super Benefits: If one spouse is older, contribution splitting allows you to transfer contributions into the older spouse’s super account. This may enable the couple to access superannuation benefits sooner, as the older spouse will reach preservation age or retirement age earlier.

Maximising Tax-Free Pension Balances: By directing contributions to the spouse who is closer to commencing a pension, you can increase the amount held in the pension phase—where earnings are tax-free. This helps optimise the couple’s overall tax position in retirement.

Reducing Tax on Super Earnings: Splitting contributions can help ensure that both spouses’ super balances stay below future tax thresholds (such as Division 296). A more even distribution of balances may reduce overall tax payable on super earnings.

Visit www.trustdeed.com.au for more details or call us on(02) 9684 4199

.png)