News | Mehak Gaba |Released: 03/06/2026 | Read: 5 Mins

With the end of the financial year fast approaching, now is the ideal time for accountants, advisers and SMSF trustees to review their fund's compliance position, complete important year-end housekeeping tasks and identify any strategic planning opportunities before 30 June.

As advisers, it is important to ensure that your clients' SMSFs remain compliant and that key year-end obligations have been addressed. A proactive review before year-end can help identify potential issues, maximise available contribution opportunities and avoid costly compliance breaches.

In this newsletter, we highlight some of the key areas that should be considered before 30 June.

1. Review your Contribution Caps including unused Carry Forward Limits

The concessional contribution cap for the 2025–26 financial year is $30,000.They are generally made from before-tax income and include:

Employer Super Guarantee (SG) contributions

Salary sacrifice contributions

Personal deductible contributions

Before making any additional contributions, members should log in to ATO Online Services via myGov and review their year-to-date concessional contributions to ensure they remain within their available cap as it will consider unused concessional contribution cap.

Opportunities for Retirees and High-Income Years

Many individuals are unaware that concessional contributions can still be made:

Up to age 67 regardless of employment status; and

After Age 67 to untill 28th day of the month after your 75th birthday , if you meet theWork Test.

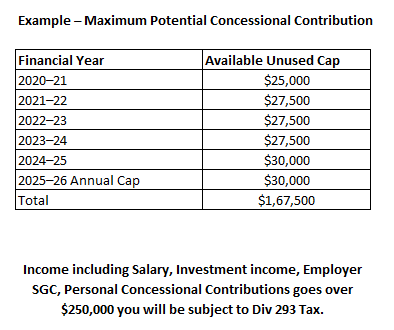

Last Chance to Use 2020–21 Unused Concessional Caps

The 2025–26 financial year represents the final opportunity to utilise any unused concessional contribution cap from the 2020–21 financial year.

Under the carry-forward contribution rules, unused concessional cap amounts can generally be carried forward for up to five years. Any remaining unused amount from 2020–21 will expire on 30 June 2026 and will no longer be available after that date.

To access carried-forward concessional cap amounts, an individual's Total Super Balance (TSB) must generally have been less than $500,000 as at 30 June 2025.

Sarah has a Total Super Balance of $420,000 as at 30 June 2025 and has accumulated unused concessional contribution cap amounts from previous financial years.

As a result, Sarah may be able to contribute up to $167,500 as concessional contributions during the 2025–26 financial year.

However, If your combined income for Division 293 purposes exceeds $250,000, an additional

15% tax may apply to some or all of your concessional contributions.

2. Review your Non-Contribution Caps including Bring Forward Rule

The Non-Concessional Contribution (NCC) cap for 2025–26 is $120,000. Non-concessional contributions are made from after-tax money and can be an effective way to increase your retirement savings within the concessionally taxed superannuation environment.

To be eligible to make NCCs, your Total Super Balance (TSB) must generally be below $2.0 million as at 30 June 2025. Importantly, individuals can generally make non-concessional contributions up , without having to satisfy the work test.

Division 296 and Spouse Equalisation Planning

With the proposed Division 296 tax targeting individuals with superannuation balances exceeding $3 million, many couples are reviewing strategies to better balance retirement savings between spouses.

For example, where one spouse has a significantly higher super balance and the other has available contribution capacity and Transfer Balance Cap space, it may be possible to:

Withdraw funds from the higher-balance spouse (where eligible).

Recontribute those funds as non-concessional contributions to the lower-balance spouse.

Commence or increase a retirement phase pension for the lower-balance spouse.

Example: John and Mary are both retired.

John's super balance is$3.8 million.

Mary's super balance is$650,000.

Mary has significant remaining Transfer Balance Cap space available.

John withdraws $120,000 from his accumulation account and contributes it to Mary's superannuation account as a non-concessional contribution.

Scenario 1 – Use the Bring-Forward Rule Before 30 June 2026

If an eligible individual triggers the bring-forward rule during the 2025–26 financial year, they may be able to contribute up to $360,000 (3 × $120,000) under the current rules.

Scenario 2 – Wait Until After 1 July 2026

From 1 July 2026, the annual non-concessional contribution cap is expected to increase to $130,000. As a result, an eligible individual may be able to trigger a new bring-forward period and contribute up to $390,000 (3 × $130,000).

3. Transfer Balance Account events in April Qtr, must be lodged by 28 July 2026.

If your SMSF has had any transfer balance account (TBA) events during the April quarter, you are required to lodge a Transfer Balance Account Report (TBAR) by 28 July 2026.

Events you need to report include: -

Commencing a retirement phase income stream.

Commencing a death benefit income stream.

Full or Partial commutations (stopping and withdrawal).

Retirement phase income streams and paying a lump sum.

Rolling back pension to accumulation phase (Stopping and not withdrawing).

If no events have occurred during the quarter, no lodgement is required. Specifically, withdrawing a pension is NOT a TBA event.

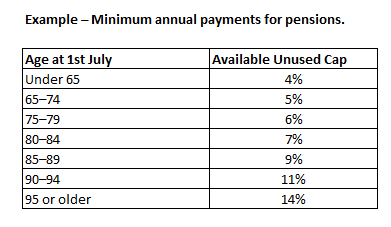

4. Minimum Pension Payments

Ensure members receiving an account-based pension have received at least the required minimum pension payment for the year. If the minimum is not paid by 30 June, the pension may be treated as having ceased for tax purposes. For transition to retirement pensions, ensure you have not taken more than 10% of your opening account balance this financial year.

John is 68 years old and has an account-based pension balance of $800,000 as at 1 July 2025.

The minimum pension percentage for a member aged 65 to 74 is 5%.

Therefore, John's minimum pension payment for the 2025–26 financial year is:

$800,000 × 5% = $40,000

If John has only withdrawn $32,000 during the year, he must withdraw an additional $8,000 before 30 June 2026 to satisfy the minimum pension requirement.

Join My Webinar- 25th June 2026!

5. Payday Super

Starts from 1 July 2026.

Employers will need to pay super at the same time as wages instead of quarterly.

Contributions will generally need to reach the fund within 7 business days of payday.

Businesses should review payroll systems, cash flow and processes before the commencement date.

Payday Super – Practical Examples

Example 1 – Current Quarterly System

ABC Pty Ltd pays its employees every fortnight.

Under the current rules, the company can pay wages throughout the quarter and then pay the accumulated Super Guarantee (SG) contributions at the end of the quarter.

For example:

Wages paid: July, August and September

Super due date: 28 October

This allows the business to hold the super contributions for several months before paying them to the employees' super funds.

Example 2 – Payday Super from 1 July 2026

ABC Pty Ltd pays employees on Friday, 10 July 2026.

Under Payday Super, the associated super contribution will generally need to be paid and received by the employee's super fund within approximately 7 business days of payday.

This means employers can no longer wait until the end of the quarter to make super payments.

6. Division 296- Proposed from 1st July 2026

From 1 July 2026, individuals with superannuation balances exceeding $3 million may be subject to an additional tax under the proposed Division 296 rules.

In simple terms:

An additional 15% tax may apply to earnings attributable to the portion of a member's super balance above $3 million.

For balances exceeding $10 million, a further 10% tax may apply.

The tax is assessed to the individual, not the SMSF.

Example – Super Balance Exceeding $10 Million

Peter has a total superannuation balance of $12 million at 30 June 2027.

Under the proposed Division 296 rules:

The portion of earnings attributable to Peter's balance above $3 million may be subject to an additional 15% tax.

The portion of earnings attributable to the balance above $10 million may be subject to a further 10% tax.

As a result, Peter could face a higher effective tax rate on a portion of his superannuation earnings compared to members with lower balances.

7. Review of In-house Assets

Review in-house assets to ensure they do not exceed 5% of total fund assets at 30 June.

If the limit is exceeded, a written plan may be required to rectify the breach.

Example – In-House Asset Breach

The Smith SMSF has total assets of $1,000,000 at 30 June 2026. During the year, the fund invested $40,000 in a related unit trust that does not satisfy the requirements of SIS Regulation 13.22C. As a result, the investment is treated as an in-house asset.

At the time of investment, the in-house asset ratio was:

$40,000 ÷ $1,000,000 = 4% which was within the permitted 5% limit.

However, by 30 June 2026:

The value of the related unit trust increased to $70,000.

The total value of SMSF assets remained $1,000,000.

As a result, the in-house asset ratio became:

$70,000 ÷ $1,000,000 = 7%

The SMSF has now exceeded the 5% in-house asset limit and has an in-house asset breach.

What Happens Next?

The trustees must:

Prepare a written rectification plan.

Take steps to reduce the in-house assets to 5% or less.

Deadline: The excess must generally be rectified by 30 June 2027.

Given the importance of these year-end matters, this newsletter provides only a high-level overview. In the coming editions, we will explore a range of additional SMSF topics in greater detail, supported by practical examples, planning opportunities and common compliance pitfalls.

Stay tuned for further insights to help you and your clients navigate the EOFY period with confidence and make informed strategic decisions.

Visit www.trustdeed.com.au for more details or call us on(02) 9684 4199