Can an SMSF segregate assets to support pension liabilities and eliminate CGT

News | Mehak Gaba |Released: 15/04/2026 | Read: 5 Mins

We understand that, in the pension phase, assets supporting retirement income streams are generally exempt from tax under the SIS Act. However, what happens if the fund’s assets are not segregated, and you decide to segregate them later after the property has already been sold? Can such segregation still be treated as supporting pension accounts?

In this newsletter, we explore the practical examples to provide a clearer understanding as it depends on the fund meeting some rules and how it’s done.

Eligibility to Segregate: S295-387 of the Income Tax Assessment Act 1997

First, it is important to determine whether the fund is eligible for "asset segregation". Not all SMSFs are permitted to use voluntary segregation. A fund will generally be restricted where, at the prior 30 June:

a member had more than $1.6m in super, and

that member was already in receipt of a retirement phase pension.

In such cases, the fund is unable to adopt the segregated method.

If fund can’t segregate the property, does it lose all tax benefits?

No, not entirely. The fund may still be entitled to a partial tax exemption on the capital gains. Where segregation is not available, the SMSF can apply the proportionate method, under which the tax-exempt portion is determined based on an actuarial certificate.

Timing is critical – no backdating allowed

A key principle in superannuation is that segregation must be:

Intended by the trustee,

Properly documented, and

Implemented at the relevant time

This means if a property has already been sold, the trustee cannot later decide to treat that asset as having been segregated to support pension liabilities.

In other words, segregation must exist at the time the asset is held and before the sale occurs not after the event.

Join my webinar on 30th April 2026

This session explores the key considerations around the segregation of assets between pension and accumulation phases, helping you better understand the rules, associated risks, and practical implications.

Cost: $50

CPD: 1 Hour

Date: 30/04/2026

CPD: 1 Hour

A cautionary note: Key Considerations

It is important to recognise that decisions must be made in advance, rather than after a property has been sold. Trustees should also be mindful that arrangements driven predominantly by tax outcomes may attract scrutiny from the ATO, particularly under the anti-avoidance provisions of Part IVA. Trustees should ensure there are genuine and supportable reasons for their actions. In particular:

Purpose of commencing a pension: Consider whether the pension was genuinely established to provide a retirement income stream, or primarily to obtain a CGT benefit. Indicators of concern may include:

The pension commencing shortly before the disposal of an asset without a clear commercial rationale.

The pension being ceased soon after achieving the intended tax outcome.

The fund being wound up shortly thereafter.

Nature of segregation Assess whether the segregation of assets is genuine and consistent with the fund’s investment strategy, rather than appearing artificial or contrived solely to obtain a tax exemption.This is particularly relevant where the fund will not be eligible to apply segregation in subsequent years, which may raise questions around the intent of the arrangement.

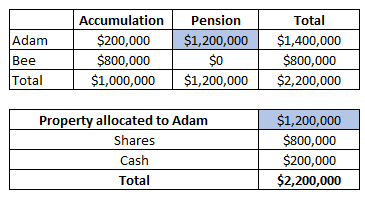

Outcomes – Where the Property is Segregated to Adam’s Pension

Where the trustee has properly implemented asset segregation and the property is held solely to support Adam’s retirement phase pension, the tax outcomes can be highly favourable.

Situation:

The SMSF (AB SMSF) is managed by a corporate trustee (AB Pty Ltd) and has two members: Adam and Bee. Adam has $200,000 in accumulation and $1,200,000 in pension phase and Bee has $800,000 entirely in accumulation. The property worth $1.2M is allocated (segregated) solely to Adam’s pension account.

Outcomes:

Income allocation: All rental income derived from the property is treated as supporting Adam’s pension interest and is therefore allocated entirely to his pension account.

Expense allocation: Similarly, all expenses relating to the property (such as maintenance, interest, and outgoings) are borne by the pension account.

Tax treatment of rental income: As the property is fully supporting a retirement phase pension (i.e., 100% in pension phase), the rental income generated from the property is exempt from income tax.

Capital gains tax (CGT) outcome: Importantly, if the property is sold while it remains a segregated pension asset, any capital gain realised on disposal will be entirely exempt from CGT.

Key Takeaways

Where an arrangement appears to be tax-driven rather than commercially justified, there is a risk that the ATO may challenge the outcome and deny the intended tax benefits.

Key takeaways:

In superannuation, decisions generally cannot be backdated. Accordingly, both the commencement of a pension and any decision to segregate assets must be made in advance.

Proper documentation is essential to support the trustee’s intent and the application of the chosen method.

The mere fact that a property is sold after a pension has commenced does not automatically mean that all, or even most, of the capital gain will be tax-free.

Visit www.trustdeed.com.au for more details or call us on(02) 9684 4199