Does Your SMSF Trust Deed Silently Void Your Client's BDBN?

News | Mansi Sharma |Released: 29/04/2026 | Read: 5 Mins

Thousands of SMSF members believe their Binding Death Benefit Nomination is permanent. For many, it is quietly lapsing every three years because of a single clause buried in their trust deed. Here's what accountants and trustees need to check today.

Under typical SMSF trust deed provisions, where a valid binding death benefit nomination (BDBN) is in place, the trustee is required to distribute the member’s death benefit in accordance with that nomination, subject to superannuation law.

However, in the absence or invalidity of a binding nomination, the position is different. The trustee retains discretion to determine how the member’s superannuation death benefit is distributed. This discretion is generally limited to:

the member’s dependants (as defined under superannuation law, including Section 302.195 of the ITAA 1997),

and/or the member’s legal personal representative.

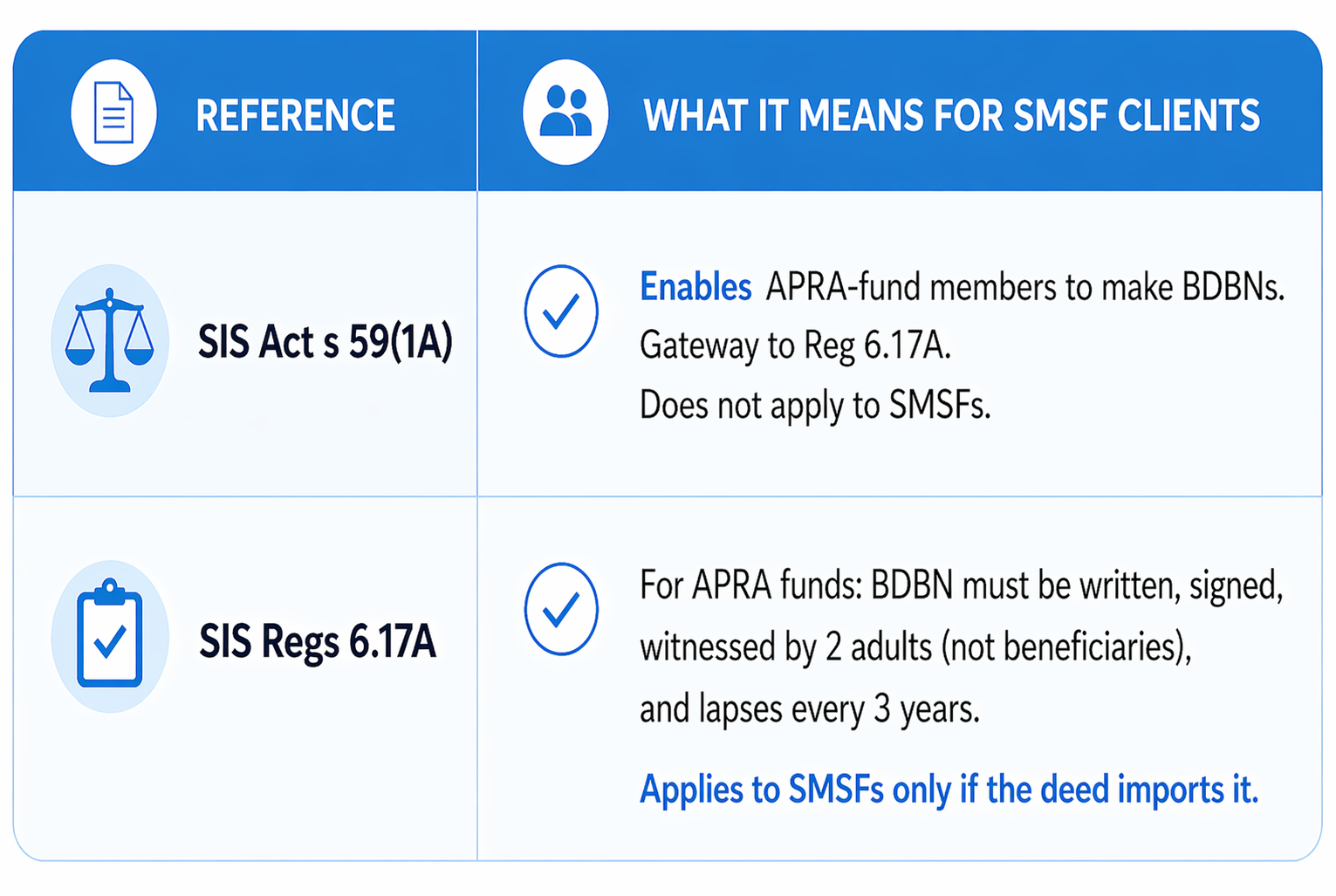

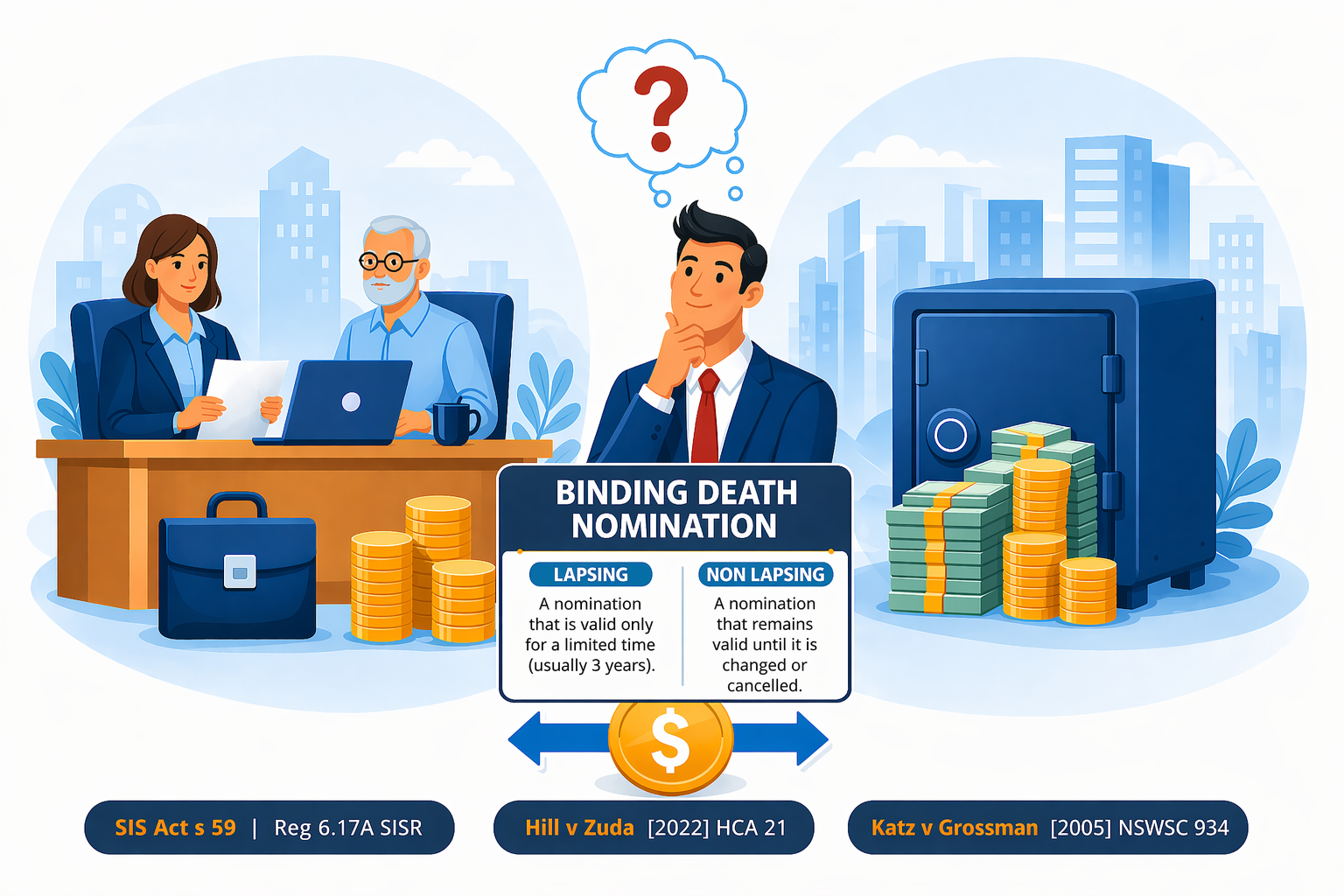

In this newsletter, we discuss the legal framework governing Binding Death Benefit Nominations (BDBNs) in SMSFs, including the relevant provisions of the SIS Act, particularly Section 59 along with Regulation 6.17A of the Superannuation Industry (Supervision) Regulations 1994 (SISR) and key case law developments.

Your client signed a BDBN. Is it still valid?

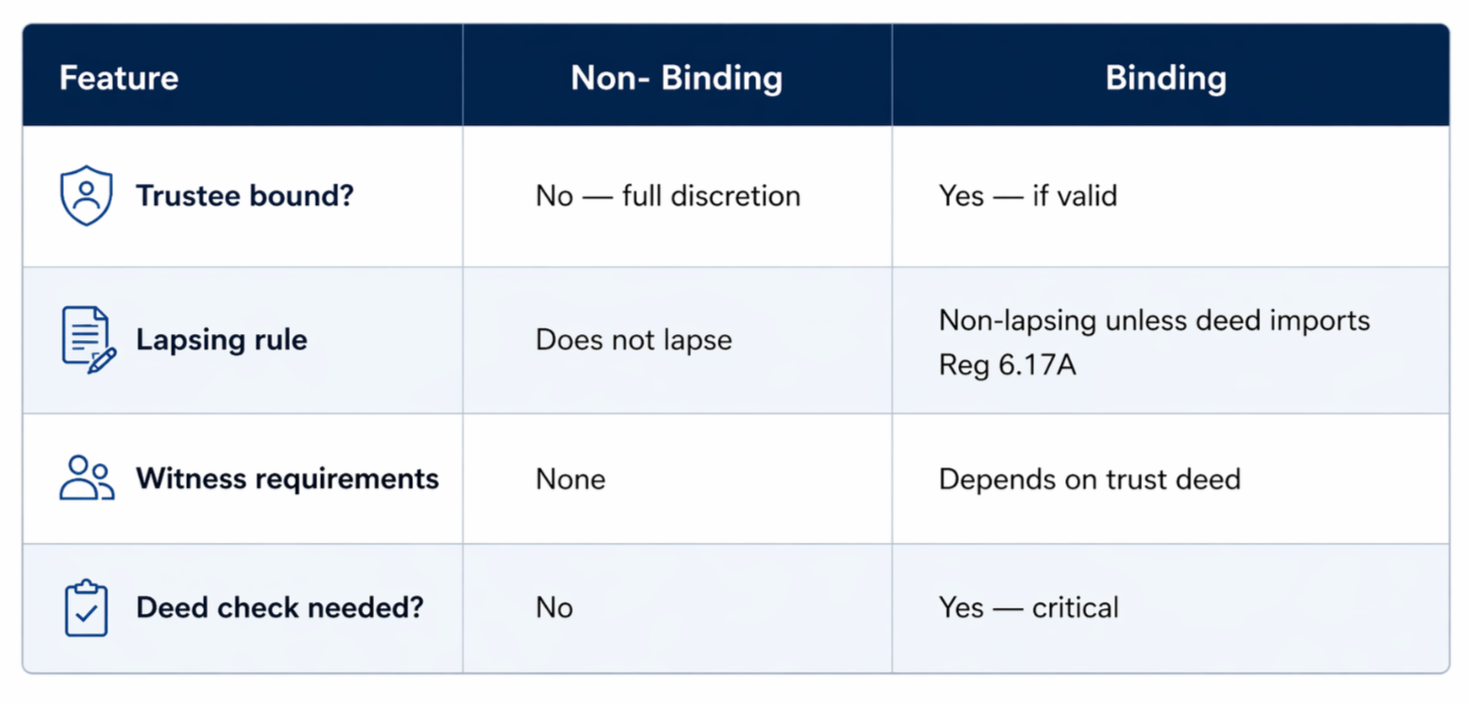

Most SMSF members know that a Binding Death Benefit Nomination (BDBN) is one of the most powerful estate planning tools available today. Unlike a non-binding nomination, which the trustee can simply ignore, a valid BDBN legally compels the trustee to pay the death benefit exactly as directed.

The problem? A significant number of SMSF trust deeds, particularly older ones, contain a clause that imports the three-year lapsing rule from Regulation 6.17A of the Superannuation Industry (Supervision) Regulations 1994 (SISR). This rule was designed for APRA-regulated funds, industry funds, retail funds and not SMSFs. Yet when a deed explicitly or implicitly adopts it, the three-year clock applies regardless.

Underlying Trust Deed Risk

Many SMSF trust deeds incorporate SIS Regulation 6.17A by reference, thereby importing the statutory three-year lapsing requirement for Binding Death Benefit Nominations. Where this occurs, any BDBN will automatically expire at the end of that period, typically without any notification to the trustee or members.

The practical consequence is significant: upon lapse, the trustee’s discretion over the distribution of the death benefit is effectively reinstated, potentially overriding the member’s original intent and creating heightened risk of dispute among beneficiaries.

Where a deed adopts this provision, it is critical that it be reviewed and, where appropriate, amended to either remove or modify the lapsing mechanism. This ensures that the fund’s estate planning framework remains aligned with the member’s intentions.

The position has been definitively settled by the Hill v Zuda Pty Ltd [2022] HCA 21.

The High Court of Australia confirmed that a binding death benefit nomination (BDBN) is not required to lapse after three years..

Where the SMSF trust deed permits a non-lapsing BDBN, the nomination remains valid until revoked or replaced.

However, if the trust deed includes a lapsing provision, the BDBN must be renewed in accordance with the deed.

Accordingly, it is essential to carefully review and strictly adhere to the provisions of the SMSF trust deed when executing a BDBN, to ensure its validity and that it effectively binds the trustee in the distribution of superannuation death benefits.

What the legislation actually says?

What Happens Without a Valid BDBN?

Ervin Katz established an SMSF and made a non-binding death benefit nomination indicating that his superannuation benefit (exceeding $1 million) be distributed equally between his daughter, Linda, and his son, Daniel.

Following Ervin’s death, Linda, as the sole remaining trustee, appointed her husband as co-trustee. The trustees subsequently resolved to allocate 100% of the death benefit to Linda, with no distribution to Daniel.

The Supreme Court of New South Wales upheld the trustees’ decision, confirming that a non-binding nomination does not impose a legal obligation on the trustee in relation to the distribution of death benefits.

This case illustrates that, in the absence of a binding direction, trustees retain full discretion in determining the allocation of SMSF death benefits, subject to the governing rules of the fund and applicable law.

Role of Non-Binding Nominations in SMSFs

Non-binding nominations do have a place in SMSFs where the remaining trustee is a trusted spouse or family member who needs flexibility around tax outcomes. The key is knowing when binding vs non-binding is appropriate for each client's specific circumstances.

Review these clients now before it's too late

Check the trust deed for Reg 6.17A : If the deed states BDBNs must comply with Reg 6.17A or lapse after three years, the deed must be amended to allow non-lapsing BDBNs. This is the single most common and costly oversight.

Ask when the BDBN was last signed. For any SMSF whose deed imports the three-year rule, nominations older than three years have already lapsed. The trustee now has full discretion.

Confirm the BDBN clearly states it is binding. Ambiguous wording might default to non-binding .

Our SMSF Deed's position on BDBN

Our SMSF deed is designed to provide both certainty and flexibility in estate planning. In case of BDBN, it allows you to incorporate a non-lapsing Binding Death Benefit Nomination (BDBN), ensuring that, upon a member’s death, the trustee is required to distribute benefits strictly in accordance with the member’s wishes.

At the same time, the deed recognises that circumstances may change. Members retain full control during their lifetime, with the ability to amend their nomination at any time—whether by converting it to a lapsing nomination or to a non-binding death benefit nomination through our SMSF tools. This balance of control, certainty, and adaptability ensures that members’ intentions are effectively preserved while allowing for ongoing review as needed.

Caution

While the High Court has simplified the regulatory side, BDBNs remain high-litigation areas. If the BDBN is not signed, dated, or delivered exactly as the Trust Deed requires, it can still be challenged and declared invalid.

Need to Update Your Client's SMSF Deed or BDBN?

TrustDeed.com.au provides Australia's most affordable SMSF trust deed updates and professionally drafted Binding Death Benefit Nominations online in minutes.

Visit www.trustdeed.com.au for more details or call us on(02) 9684 4199

.png)