How to avoid getting caught in the in-house asset trap?

News | Mehak Gaba |Released: 06/05/2026 | Read: 5 Mins

In-house asset rules are highly technical in nature. In simple terms, an in-house asset arises when an SMSF invests in or deals with a related party, such as members, their relatives, or entities they control. The law places a strict limiton these investments — the total value of in-house assets must not exceed 5% of the fund’s total assets on 30th June each year.

There are also specific rules about what you can and can’t do with your SMSF investments. The rules not only relate to the actual nature of the investments but also who you buy them from and what you can do with them once your SMSF owns them.

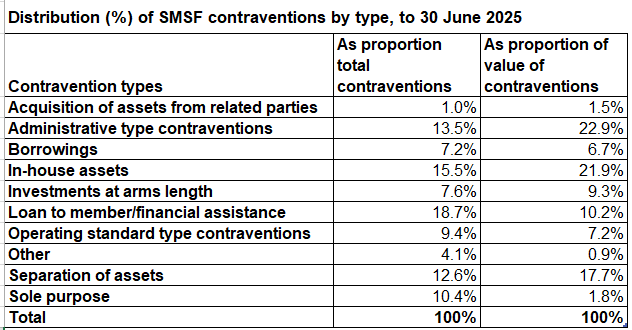

In-house assets remain one of the most common contraventions reported to the Australian Taxation Office through Auditor Contravention Reports (ACRs). In most financial years, it ranks as the second most reported breach. The table below outlines the various types of contraventions reported to the ATO by SMSF auditors since the start of contravention reporting upto 30 June 2025.

What is In-house assets? Who is Related party?What are the rules?

Subsection 71(1)of the Superannuation Industry (Supervision) Act 1993defines what constitutes an in-house asset of the fund that is:

A loan to, or an investment in, a related party of the fund

An investment in a related trust of the fund

An asset of the fund subject to a lease or lease arrangement between a trustee of the fund and a related party of the fund.

Section 10 of the Act‘Related party’ also has a very specific definition under SIS law and is any of the below:

A member of the fund

A standard employer-sponsor of the fund

A Part 8 associate of one of the above.

What are the rules?

There are lot of rules around transcations between Self managed Super Funds and Related parties. This is to ensure that funds are run for sole purpose of providing super benefits to members when they retire.

This means trustees, members, relatives and other related entities of fund cannot get any immediate or present day benefit outside that purpose.

Loan or Financial Assistance

Suitation: Meet Tony- Tony is the only member of his SMSF. Ryan is his son and Kelly is his sister. Ryan wants to buy his first home. He asks Tony, if he can borrow money from Tony's fund for his deposit and use the fund's assets as security for the home loan.

Solution: Both of these options are strictly prohibited. SMSFs are not allowed to loan money or provide financial assistance to members or their relatives.

Selling Assets

Suitation: If Ryan wanted to buy a property from Tony's SMSF, it would not to be at market value.

Solution: An SMSF can't sell an asset to a related party if the transcation is not on commercial terms.

Lease the property

Situation: Ryan wants to lease a property owned by Tony’s SMSF. However, the value of the property exceeds 5% of the fund’s total assets, making it an in-house asset.

Solution:Tony’s SMSF cannot lease the property to Ryan, as this would breach the 5% in-house asset limit.

Acquiring Assets from Related Parties

Situation:Tony’s SMSF wants to purchase a residential unit owned by his sister Kelly (a related party).

Solution: SMSF are not allowed to acquire assets from related parties, So Tony's fund would not be able to purchase a residential unit that his sister kelly owned. This is prohibited. There are few exceptions, such as:

Business real property.

Listed securities.

Units in trusts that are considered ‘widely held’ (for example, managed funds, certain unlisted property trusts with a large number of investors).

There are a few others but these are the most common.

Collectable Assets

Situation: Kelly offers to store the SMSF’s artwork at her home. As a related party, this would mean the fund’s collectable asset is being stored or used by a related party.

Solution: Tony declines the offer and arranges for the artwork to be kept in a secure, independent storage facility. SMSF collectable assets cannot be stored, leased, or used by related parties, as this is prohibited.

Tip: If you are unsure what's allowed, you should contact an SMSF professsional to help you get it right.

Join my webinar on 21st May, 2026- In-House Assets Rule

Date: May 21 , 2026

Time: 4:30 PM- 5:30 PM AEST

CPD: 1 Hour

Cost: $50

Our next 2–3 newsletters will focus exclusively on in-house assets. We’ll cover in-house asset rules in the context of LRBAs, how to calculate the 5% limit, practical examples, and much more to help you better understand and manage compliance.

What approach an auditor should take?

When auditing in-house assets, the auditor’s main job is to check the below points:

Check whether your SMSF has stayed within 5% in-house asset limit as of 30th June.

Reviewing your fund’s financial statements to confirm themarket value of total assetsas of 30 June.

Examines documents related to loans, related-party trusts, related companies, and any property leased to related parties. They look for proper agreements, valuations, repayment terms, and evidence that transactions were made on normal commercial conditions.

If in-house assets exceed 5%, the auditor must verify that the trustee has prepared a written rectification plan within the required timeframe, that the plan is realistic, and that appropriate steps have been initiated to bring the fund back within the limit.

SIS Act may impose various administrative penalties for in-house asset breaches, including fines of up to 60 penalty units on trustees. In serious cases, this may also lead to the loss of the fund’s complying status or the disqualification of trustees, along with other potential penalties.

Overall, an SMSF auditor ensures that your fund is protecting member money and following ATO rules without any hidden risks.

Visit www.trustdeed.com.au for more details or call us on(02) 9684 4199