Regulation 13.22C unit trusts – Opportunity or Burden?

News | Mehak Gaba |Released: 14/05/2026 | Read: 5 Mins

Let’s say you have a successful business, AB Pty Ltd, and the business now needs a larger commercial premises to expand. However, purchasing the property may be beyond your personal capacity or your SMSF balance on its own.

Normally, this creates a problem because under the in-house asset rules, an SMSF is generally not allowed to heavily invest in a related trust or company beyond 5% of the total SMSF assets.

However, there is an important exception under Regulation 13.22C of the SIS Regulations. This allows an SMSF to invest up to 100% in a complying ungeared unit trust without breaching the in-house asset rules.

This can be a very effective strategy for acquiring commercial property, especially where both personal and SMSF funds are combined. However, the rules are extremely strict.

In this newsletter, we explore this strategy to provide a clearer understanding of how this strategy works.

Practical example of how this strategy works:

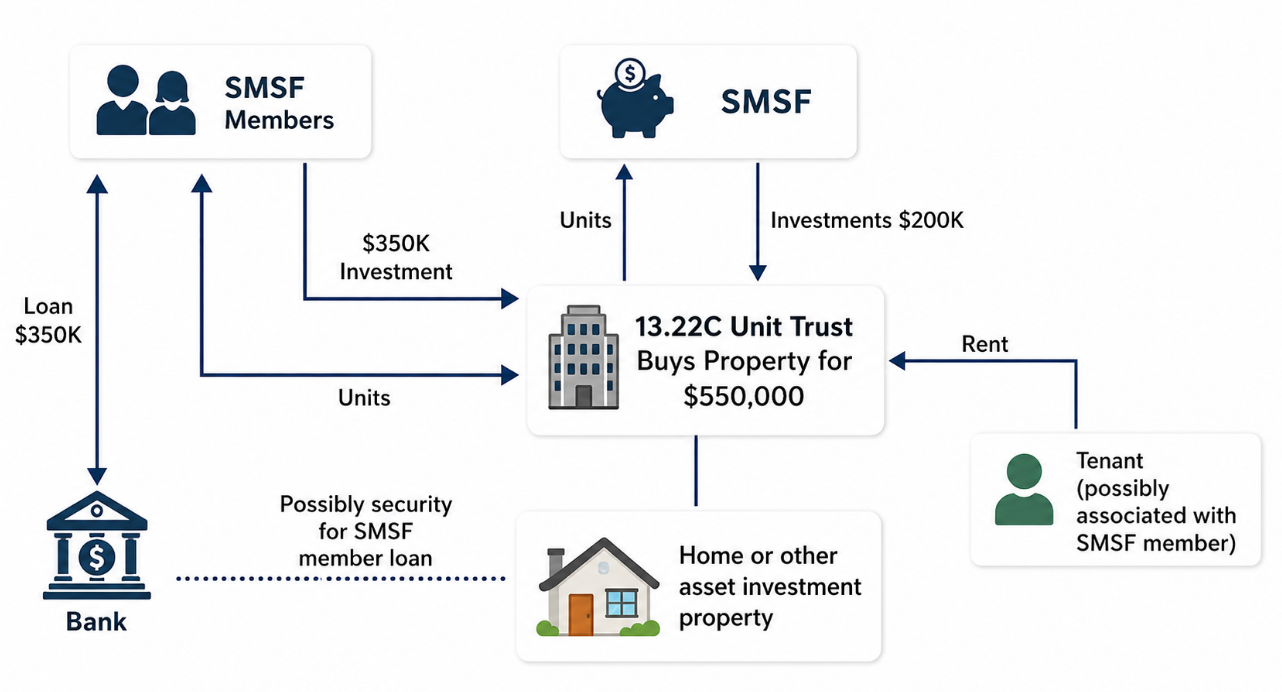

A & B use both their SMSF money and personal money to buy a commercial property through a 13.22C Unit Trust.

SMSF invests: $200K

Personally they invest: $350K

Total property investment: $550K

The Unit Trust buys the property and receives rent from the tenant. Profit is shared based on ownership:

SMSF gets 36%

A & B personally get 64%

This is not possible when a Self Managed Super Fund and related party co-own a property as tenants in common unless it is business real property and basic criteria of Regulation 13.22C are properly followed.

The Basic criteria of Regulation 13.22C

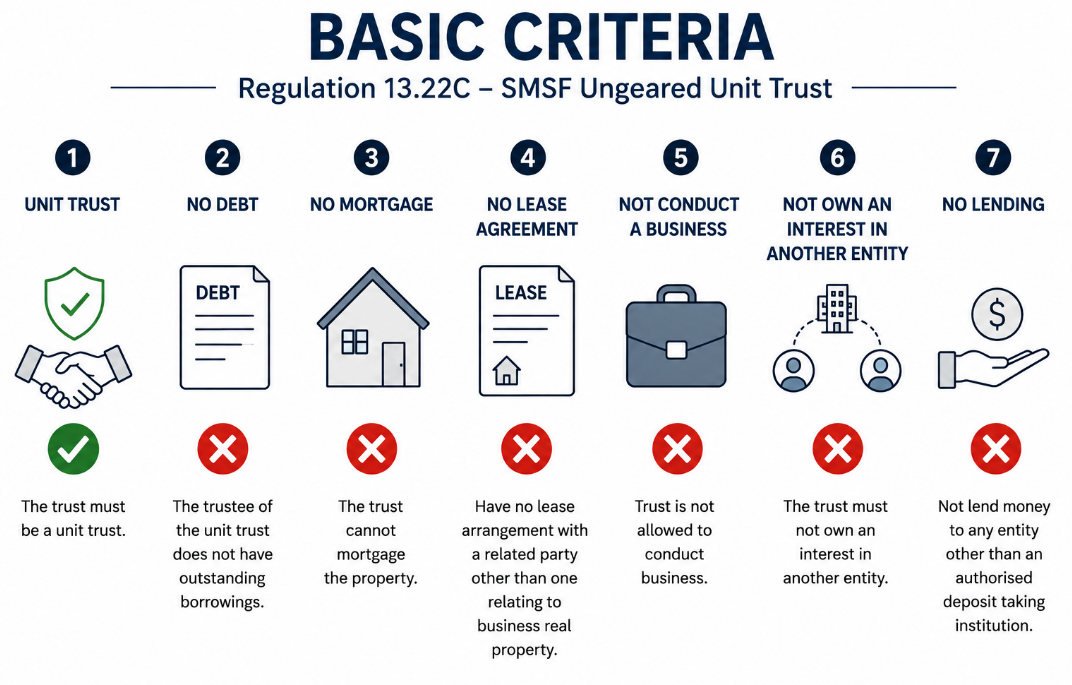

To meet the requirements of SIS regulation 13.22C, the trust must:

Be a unit trust;

Have no debt and not allow any security to be taken over its assets;

Have no lease arrangement with a related party other than one relating to business real property;

Not acquire an asset (other than business real property) from a related party;

Not lend money to any entity other than an authorised deposit taking institution (eg, a bank);

Not conduct a business. Therefore, depending on the size and scale of the development, the trustee should consider engaging a third party to develop the land for a fee.; and

Not own an interest in another entity – which means it cannot own shares or invest in another trust.

Broadly, this means the trust will only own residential or business real property and cash on deposit.

Join my webinar on 21st May, 2026

Key topics covered:

Understanding how SMSFs can invest in certain related trusts or companies that meet the requirements under section 13.22C.

Rules and restrictions when acquiring assets from members or related parties includingLoan or Financial Assistance, Selling Assets, Leasing the property and Collectable Assets.

Calculation of 5% limit through practical examples.

Important checks trustees should keep in mind to avoid breaching in-house asset rules.

If Criteria of Regulation 13.22C are not satisfied

As mentioned above if any of the conditions in Regulation 13.22C are not satisfied, the SMSF’s units in the unit trust will be treated as an in-house asset of the SMSF and the in-house exception in Regulation 13.22C cannot be subsequently applied even if the breach is rectified (refer toRegulation 13.22D(3)).

Some common traps within this area that lead to the units being an in-house asset include:

The trustee of the unit trust acquires any interest in another entity, even (for example) listed securities.

The trustee of unit trust makes a loan to another entity other than a deposit with an authorised deposit-taking institution. This means a deposit with any non-approved institution will trigger reg 13.22D.

The trustee of the unit trust borrows money.

A charge or mortgage is given over an asset of the unit trust.

The trustee of the unit trust conducts a business. There is no exception for conducting a business of property development, so people doing any developments with real estate must be extremely careful.

The trustee of the unit trust leases one of its assets to a related party, unless the asset is business real property. A triggering event may also occur if the property loses its status as business real property.

Key Takeaways

A trustee of an SMSF who invests in Unit Trust should check that all the criteria in reg 13.22C are satisfied prior to making the initial investment. Care should also be taken to ensure that no events under reg 13.22D occur. Where there is doubt or uncertainty as to the application of the relevant law, it is recommended that expert legal advice be obtained.

Visit www.trustdeed.com.au for more details or call us on(02) 9684 4199