News | Mehak Gaba |Released: 20/05/2026 | Read: 5 Mins

Under Section 66 of the SIS Act, a self-managed super fund (SMSF) is generally prohibited from acquiring assets from related parties. The purpose of Section 66 is to prevent trustees from:

transferring personal assets into an SMSF inappropriately

using the SMSF for personal benefit

dumping poor-quality or non-compliant assets into super

gaining illegal early access to superannuation benefits

However, there are important exceptions to this rule where acquisitions from related parties are permitted. For example, an SMSF may acquire business real property from a related party if the acquisition satisfies the SIS Act requirements. In contrast, transferring residential property owned by a related party into an SMSF is generally prohibited.

Defination of Section 66 of SIS Act, 1993

Under s66 SIS Act, an SMSF must not intentionally acquire an asset from a related party. Some exceptions exist. They come with the mandatory condition that an SMSF must acquire these assets at market value in line with r8.02B SISR:

Listed shares on an approved stock exchange or licensed market.

Business real property (BRP).

An in-house asset (IHA) that does not result in acquiring more than 5% of the fund’s assets.

Other assets excluded from being an IHA unders71 SIS, such as widely held trusts and r13.22C trusts.

Life insurance policy from a related party (not from a member or relative of the fund).

Relationship breakdown.

Let’s understand through practical examples in SMSFR 2010/1

Example 1: Acquisition of listed units in a unit trust

Pina, a member and trustee of the Syd SMSF, owns units in a unit trust which is listed on the Australian Securities Exchange. Pina sells the units to the SMSF. Market value consideration is paid for the units. The units are listed securities as defined in subsection 66(5).

A trustee or investment manager of the Syd SMSF does not contravene subsection 66(1) by purchasing the units from Pina as they are listed securities and the market value requirement is satisfied.

Example 2: Acquisition of fixtures forming part of land that is business real property

Adam is a member and a trustee of the AAA SMSF. Adam owns a commercial property consisting of land and a factory where he operates his business. Adam sells this property to the AAA SMSF. Market value consideration is paid for the property.

The SMSF acquires the freehold interest in the land, which includes the factory and other things that are fixtures on that land. The freehold interest in the land satisfies the definition of business real property.

As it is the acquisition of business real property and market value consideration is paid, the acquisition does not contravene subsection 66(1) provided the SMSF has fewer than five members.

Example 3: Acquisition of shares in a company that is a related party

Michael and Catherine are members and trustees of the J.J. SMSF. They each hold 500 shares in an unlisted company that is a related party of the SMSF.

Catherine wants to contribute her 500 shares to the SMSF and so transfers the shares to the SMSF for no consideration. As the shares constitute investments in a related party of the SMSF the shares satisfy the requirement in subparagraph 66(2A)(a)(i).

A trustee or investment manager of the J.J. SMSF can acquire the shares without contravening subsection 66(1) if the other requirements of subsection 66(2A) are satisfied. That is, the shares are treated by the SMSF as a contribution equal to the shares’ market value at the time when the shares are acquired and the acquisition of the shares does not cause the SMSF to exceed the 5% permitted level of in-house assets. The shares are acquired when the (trustee(s) of the SMSF becomes the owner of the shares.

Example 4: Acquisition of units in a related unit trust

Audrey is a member and a trustee of the Jones SMSF. Audrey holds 1,000 units in a unit trust that is a related trust of the SMSF and is not a widely held unit trust.

Audrey sells 200 units to the Jones SMSF. Market value consideration is paid for the units. As the units constitute investments in a related trust the units satisfy the requirement in subparagraph 66(2A)(a)(i).

A trustee or investment manager of the Jones SMSF can acquire the units without contravening subsection 66(1) if the other requirements of subsection 66(2A) are satisfied. The market value requirement in paragraph 66(2A)(b) is satisfied as the units are acquired for market value consideration. Therefore, provided the acquisition of the units does not cause the SMSF to exceed the 5% permitted level of in-house assets the requirement in paragraph 66(2A)(c) is also satisfied and the units can be purchased without contravening subsection 66(1).

Join my webinar on 28th May, 2026

Key topics covered:

Section 66 and its exceptions.

Understanding how SMSFs can invest in certain related trusts or companies that meet the requirements under section 13.22C.

Rules and restrictions when acquiring assets from members or related parties includingLoan or Financial Assistance, Selling Assets, Leasing the property and Collectable Assets.

Calculation of 5% limit through practical examples.Important checks trustees should keep in mind to avoid breaching in-house asset rules.

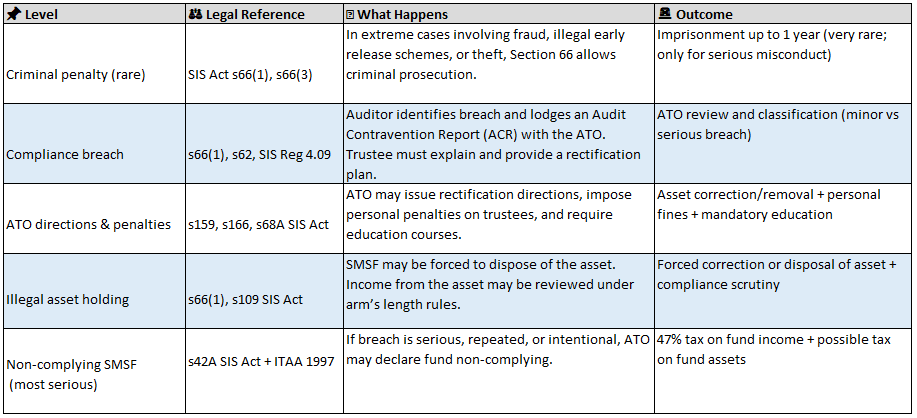

What happens if the rules are breached?

Visit www.trustdeed.com.au for more details or call us on(02) 9684 4199