100% versus 5% in-house asset limit on in-house assets.

News | Mehak Gaba |Released: 27/05/2026 | Read: 5 Mins

As accountants and advisers, it is important to review whether your client’s SMSF acquisitions and investments comply with the in-house asset rules. Where an SMSF acquires assets or enters into arrangements with related parties, understanding these rules is essential to determine whether thefund can invest up to 100% in an eligible asset or whether the investment will be subject to the strict 5% in-house asset limit.

Generally, an SMSF may invest up to 100% in certain related-party investments where a specific exception applies and the investment is not treated as an in-house asset. Common examples include investments in a Custodian Trust, Widely Held Unit Trusts, Business Real Property leased to a related party, and investments in related trusts or companies that satisfy the requirements of SISR 13.22C.

However, where the investment is considered an in-house asset, the SMSF is limited to invest up to 5% of the total fund assets. Now, the important question is what is considered as In-house assets and what is not considered as In-house assets ?

In this newsletter, we briefly break down the in-house asset provisions, key exceptions, and the practical issues accountants should be aware of when reviewing SMSF investments.

Understanding In- House Assets in an SMSF

Section 71 of SIS Act broadly defines an in-house asset of a superannuation as:

An asset of the fund, that is:

· A loan to a related party of the fund;

· An investment in a related party of the fund;

· An investment in a related trust of the fund; or

· An asset of the fund that is subject to a lease or lease arrangement with a related party.

In simple terms, if your SMSF is “investing in or doing business” with someone closely connected to the members or the trustees of the fund, it is likely that the investment to be an in-house asset. And if funds breach the in-house asset rules then the fund’s auditor is obliged to report the breach to the regulator, namely ATO.

Assets that are NOT In–House Assets

Not every investment or arrangement involving a related party will automatically be treated as an in-house asset. The superannuation legislation provides a number of important exclusions and exemptions, which means an SMSF may, in certain circumstances, invest up to 100% in these assets without breaching the in-house asset rules.

Some common examples where up to 100% investment may be permitted include:

1. Life Insurance Policies : A life insurance policy issued by a registered life insurance company.

2. Bank Deposits: Money held as a deposit with an ADI (Authorized Deposit-Taking Institution) for example, a bank term deposit.

3. Assets Specifically Approved by the Regulator: If the regulator (usually the ATO for SMSFs) issues:

· A written notice, or

· A legislative instrument

stating that an asset is not an in-house asset;

4. Business Real Property (e.g. shop, office or factory etc.) Leased to a Related Party: A business real property, and leased to a related party on proper legal terms;

5. Investment in a Widely Held Unit Trust: A widely trust is a fixed unit trust with fixed entitlements to the income & capital of the trust.

6. Property Held as Tenants in Common: If a SMSF and a related party jointly own property (as tenants in common), & it is not leased to the related party, it is not an in-house asset (remember no borrowing).

7 . Investment in SISR 13.22C Trusts: There are some special type of trusts which do not borrow and hold assets and only a bank account.

8. Where SMSF invests in a Custodian Trust: These are some special trusts which are created as property custodians when the SMSF borrows aka Bare Trusts.

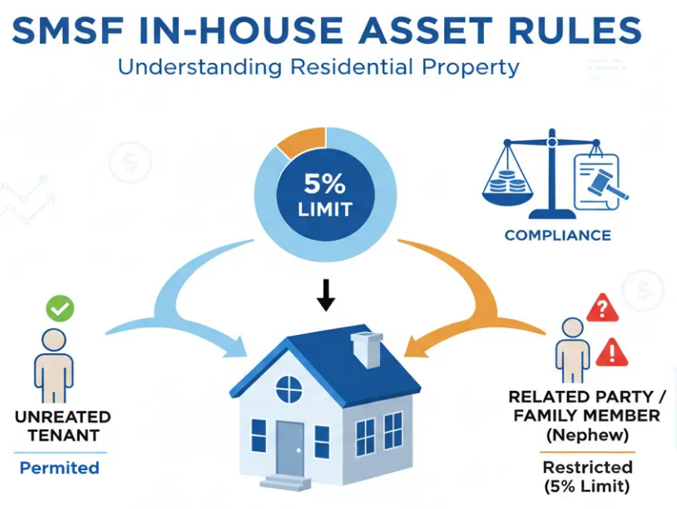

Example 1: To Understand the Exemption

Residential Property leased to Related Party

An SMSF owned a residential property which was previously leased to an unrelated tenant. After the lease ended, the trustees considered leasing the property to the nephew of a fund member. Generally, residential property leased to a related party becomes an in-house asset under the SIS Act. Therefore, the SMSF would need to calculate whether the value of the property breaches the 5% in-house asset limit.

CRUX: A residential property leased to a related party will generally be treated as an in-house asset, even if the property was originally acquired from an unrelated party. In contrast, business real property may be leased to a related party without being classified as an in-house asset, provided the arrangement is maintained on arm’s length terms.

Example 1: To Understand the Exemption

Investment in a Related Unit Trust

An SMSF invests in units of a related unit trust. The trust has borrowed money to acquire assets. Because the trust is geared (borrowed), the investment will generally be treated as an in-house asset. If the value of the investment exceeds 5% of the total market value of the SMSF’s assets, the fund may breach the in-house asset rules.

However, if the related trust satisfies the requirements of a SISR 13.22C trust — meaning, among other things, that it does not borrow and complies with strict legislative conditions — the investment will not be treated as an in-house asset. In that case, the SMSF may invest more than 5%, and potentially even 100% of the fund’s available cash, into the trust.

CRUX: A related trust or company that has borrowings will generally be treated as an in-house asset and be subject to the strict 5% limit. However, where the entity qualifies as a compliant SISR 13.22C non-geared trust or company, the SMSF may invest up to 100% without breaching the in-house asset rules.

How is 5% In-House Asset measured & how can a breach be Rectified?

All SMSF Auditors check the 5% limit of in-house assets at the end of each financial year.

The fund must calculate the market value ratio of its in-house assets (basically, the percentage of the fund’s assets that are loans, investments, or leases with related parties) divided by the market value of all assets of the fund.

If this ratio is more than 5%, then the fund is considered to breach the 5% rule. Then the Trustees must take some action to resolve or to fix this breach.

Action 1: The trustee of the fund must prepare a written plan; This plan must show steps how the trustees propose to reduce the excess amount (above 5% limit):

One or more of the funds -inhouse assets held at the of the year are disposed of during the next following year and

The value of the assets so disposed of is equal to or more than the excess amount

This plan should be prepared before the end of next year and each Trustee of the fund must ensure that the steps in the plan are carried out.

Key takeawys

Confusing? Even well-intentioned trustees can unintentionally breach the 5% in-house asset rules through loans, investments, or lease arrangements involving related parties. The consequences of a breach can be significant and may include rectification plans, Auditor Contravention Reports (ACRs), ATO penalties, the fund being made non-complying, and potentially the loss of the fund’s concessional tax treatment.

Accordingly, trustees should seek professional advice before entering into any investment or related-party arrangement within an SMSF.

Join My Webinar tomorrow!

Visit www.trustdeed.com.au for more details or call us on(02) 9684 4199