Tax Rules Tighten, Superfunds are still taking Centre Stage

News | Mehak Gaba |Released: 18/06/2026 | Read: 5 Mins

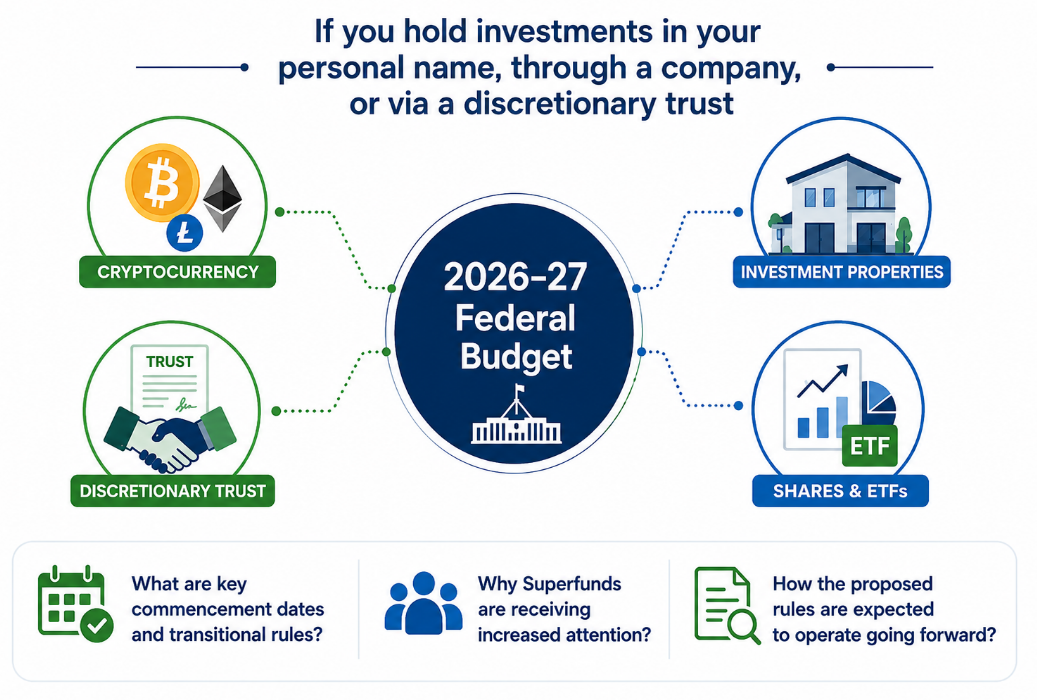

If you hold investment properties, shares, ETFs, cryptocurrency, or invest through a discretionary trust, please note that the 2026–27 Federal Budget may significantly affect your long-term investment and tax planning strategy.

For many years, Australian investors have relied on three key tax concessions to help build wealth:

Negative gearing on investment properties.

The 50% Capital Gains Tax (CGT) discount on assets held for more than 12 months.

Flexible income distribution through discretionary trusts.

The Government has now proposed significant reforms in each of these areas, including:

Limit negative gearing to claim tax concession from 1st July 2027.

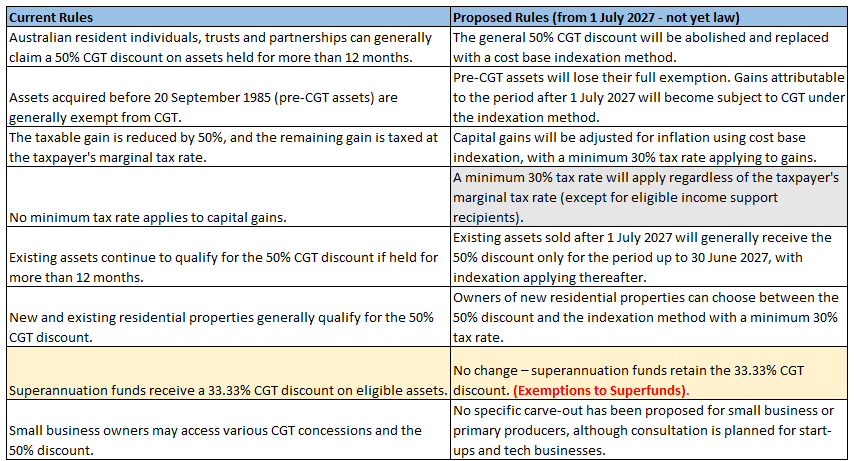

Replace the 50% Capital Gains Tax (CGT) discount for individuals, trusts and partnerships with cost base indexation and a 30% minimum tax rate on capital gains accruing from 1 July 2027.

Introducing a 30% minimum tax on discretionary trusts from 1 July 2028.

As a result, investors may need to REASSESS THETYPE OF ENTITY how and where they hold their investments moving forward. In this newsletter, We will provide a brief overview of the proposed changes? What are key commencement dates and transitional rules? Why Superfunds are receiving increased attention ?

Negative Gearing Rules Tighten for Property Investors

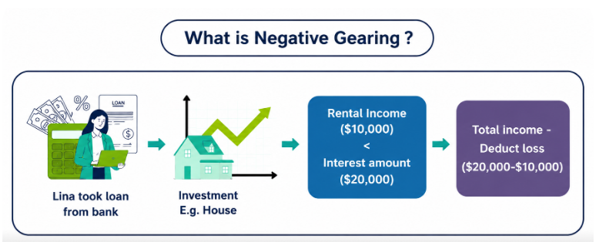

Current Negative Gearing Rules through an example

Lina earns $85,000 per year and owns an investment property. The property generates $10,000 in rent but incurs $20,000 in expenses, resulting in a $10,000 loss.

Under the current rules, this loss can be offset against her other income, reducing her taxable income to $75,000 and lowering her tax payable. These rules are proposed to change from 1 July 2027.

Proposed Negative Gearing Rules

Before applying negative gearing, check the following:

When was the property acquired? - Dates are very important !

Is it a commercial property, new residential build, or established residential property?

Under what structure is the property held (individual, trust, SMSF, or partnership)?

Scenario 1 –Property owned (or under contract) before 7:30pm AEST on 12 May 2026.

✅ Negative gearing continues indefinitely under the existing rules (Grandfathered). Any rental losses can continue to be offset against salary and other taxable income, even after 1 July 2027. NOTHING CHANGES.

Scenario 2 – Property acquired between 12 May 2026 and 30 June 2027

✅ Negative gearing remains available until 30 June 2027.

❌ From 1 July 2027, rental losses can no longer be offset against salary and other income.

Scenario 3 – Property purchased on or after 1 July 2027

❌ Negative gearing is generally not available.

But there are new exemptions:

eligible new builds (to increase housing stock).

properties held by widely held trusts and superannuation funds. (Exemption on SUPERFUNDS)

targeted build-to-rent developments and private investors supporting government housing programs.

Losses from established residential properties:

will only be deductible against rental income or the capital gains from residential properties

can be carried forward and offset against residential property income in future years.

Proposed 30% Minimum Tax on Discretionary Trust- 1st July 2028

Current Rules through an example

Trust income: $200,000

Split (individual beneficiaries):

Husband: $50k

Wife: $50k

2 kids: $50k each

👉 Each person taxed separately → lower total tax. Each person is taxed at their own marginal tax rate.

Why it matters?

The proposed Budget states that the “growing use of discretionary trusts is increasingly unsustainable” and supports this with the following data:

Discretionary trusts have doubled since 2001–02, growing faster than companies (+70%).

Australia now has 1M+ trusts; ~80% are discretionary trusts.

In 2022–23, they distributed $142.4B income, growing ~7.8% annually since 2011–12.

Most trust income goes to the top 10% of earners.

~90% of private trust wealth is held by the wealthiest 10% of households (net worth > ~$2.3M).

Proposed Changes

A 30% minimum tax will apply to the taxable income of discretionary trusts and will generally be paid by the trustee.

Beneficiaries, excluding corporate beneficiaries, will receive non-refundable credits for the tax payable by the trustee.

A 30% floor — not a cap this means that if a beneficiary’s effective tax rate is above 30 percent, they will still need to pay additional tax, while those taxed below 30 percent will not receive a refund for the difference.

Expanded rollover relief will be available for three years from 1 July 2027 to support small businesses and others that wish to restructure into another entity type.

The proposed rules do not apply to SUPERFUNDS (Exemptions on Superfunds) and other complying superannuation funds, Fixed and widely held trusts, Charitable trusts, Special disability trusts, Deceased estate.

Abolition of the CGT Discount

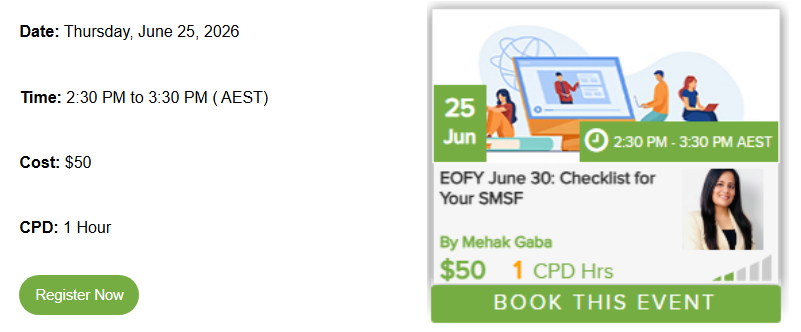

Join My Webinar- 25th June 2026!

Why are SMSFs standing out?

Recent proposed tax reforms have made SMSFs increasingly attractive, as many of the changes do not apply to complying superannuation funds.

CGT Concessions Remain: SMSFs are expected to retain their existing one-third CGT discount on assets held for more than 12 months, while individuals and trusts may lose access to the current 50% discount.

Exempt from Negative Gearing Changes: Proposed negative gearing restrictions are not expected to apply to SMSFs, allowing them to continue operating under the current rules.

Excluded from the Proposed 30% Trust Tax: The proposed minimum 30% tax rate for discretionary trusts from 1 July 2028 will not apply to complying superannuation funds.

Concessional Tax Environment: Investment earnings in an SMSF are generally taxed at a maximum rate of 15% in accumulation phase, with potential tax-free earnings in retirement phase.

As tax rules tighten for individuals and discretionary trusts, SMSFs continue to offer a highly tax-effective environment for long-term wealth creation.

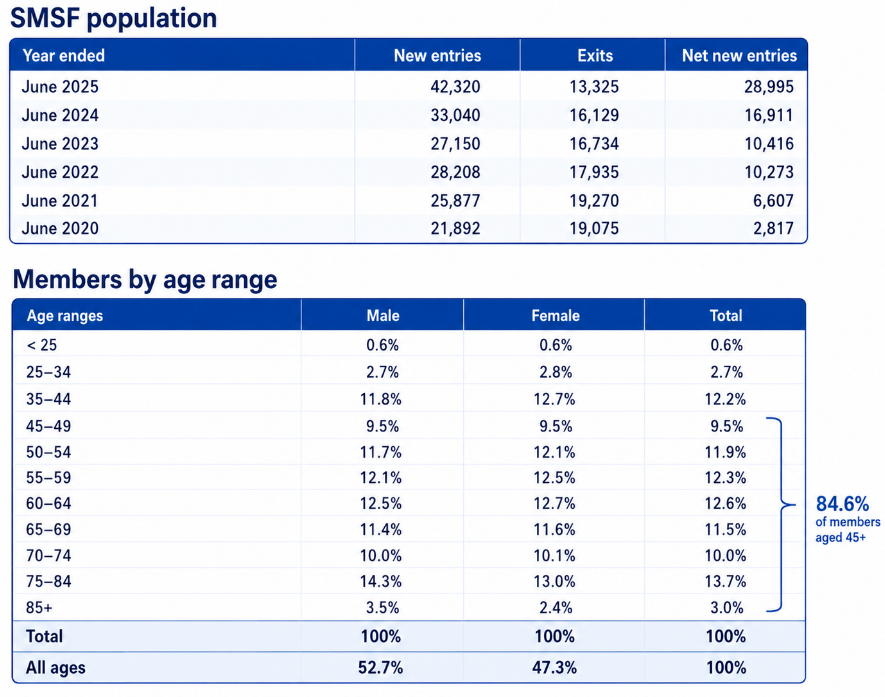

The SMSF demographics are also quite revealing. During the year ended June 2025, approximately 42,230 new SMSFs were established, compared to 33,040 in the year ended June 2024 (28% growth in new SMSF establishments).

According to the latest ATO statistics, approximately 84.6% of SMSF members are aged 45 and over with average assets per SMSF of approx. $1.63 million.The data highlights that SMSFs continue to be a preferred vehicle for managing and growing substantial investment portfolios.

Suppose, if you purchase an investment property through your SMSF and hold it for 10–15 years, any rental income earned during the accumulation phase is generally taxed at a maximum rate of 15%. If the property is sold after retirement, any capital gain on the sale may be completely tax-free, subject to the applicable superannuation rules and transfer balance cap limits. This can result in a significantly lower tax outcome compared to holding the same property in any other entity.

This strong growth demonstrates increasing confidence in SMSFs as a vehicle that offers greater control, flexibility, and strategic planning opportunities for investments and retirement savings.