Implications for the Auditor’s Report where Use of Going Concern Basis of Accounting is Inappropriate such as for an Self Managed Super Fund.

When the use of the going concern basis of accounting is appropriate, assets and liabilities are recorded on the basis that the entity will be able to realise its assets and discharge its liabilities in the normal course of business.

Some SMSF auditors may agree that Auditing standard ASA 570 "Going Concern" concept does not apply to Self Managed Super Funds.

Under the going concern basis of accounting, the financial report is prepared on the assumption that the entity is a going concern and will continue its operations for the foreseeable future.

General purpose financial reports are prepared using the going concern basis of accounting, unless management either intends to liquidate the entity or to cease operations, or has no realistic alternative but to do so. However, SMSF financial reports are special purpose reports and not general purpose financial reports.

Should SMSF Financial Statements be prepared as a "Going Concern"

SMSF financial reports are special purpose financial reports and the trustees may or may not decide to prepare financial statements in accordance with a financial reporting framework for which the going concern basis of accounting is relevant.

1) As per paragraph 2 of ASA 570 The going concern basis of accounting is not relevant for some financial reports that are prepared on a tax basis in particular jurisdictions such as SIS Regulations.

2) Since any (or all) trustees can die at any time and their death benefit paid out compulsorily to beneficiaries, in particular Subregulation 6.21(1) of the SISR provides that a member's benefits in a regulated superannuation fund must be 'cashed' as soon as practicable after the death of the member (or the benefits are rolled over as soon as practicable for immediate 'cashing', in accordance with subregulation 6.21(3) of the SISR).

3) ATO ID 2015/23 suggests that Member's benefits in a regulated superannuation fund must be 'cashed' upon death by being paid - mere journal entries to credit beneficiaries in the same fund are insufficient.

4) Subregulation 6.21(2) of SISR goes on to prescribe the form in which the benefits may be cashed for the purposes of regulation 6.21 of SISR, subject to the additional restrictions in subregulations 6.21(2A) and (2B) of the SISR.

5) In accordance with paragraph 6.21(2)(a) of the SISR, the benefits may be paid by being cashed as a single lump sum (or an interim and final lump sum).

This means that an SMSF can continue as a "going concern" only on the condition that the dependents decide the deceased members amount to be paid out to them as a death benefit pension. Please note that some dependents, like children cannot continue these death benefit pensions, once they become adults.

From the above our understanding is that SMSF financial statements must be prepared as if it is an entity which is to be liquidated and where going concern concept is not to be applied.

Current Situation

What we have witnessed in the recent past is that reviewers from professional bodies insist that the SMSF auditor includes in his checklist audit procedures to check on the going concern capability of an SMSF. Auditors are being asked by reviewers to evaluate trustees procedure of examining the SMSF's going concern ability in the financial statements and design their own checklist and audit procedure to check if the financial statements are prepared under the going concern accounting framework and document these audit procedures in their working papers.

We believe that a declaration (assertion basis of auditing) by the trustees in their representation letter to the auditor is sufficient assurance to the auditor that the fund is a going concern and a solvent fund.

A few SMSF auditors who use our system have recently been targeted by reviewers on lack of audit procedures in our system on the below three issues, in response, we have enhanced our checklist to include these issues.

a) Going concern

b) subsequent events after balance date

c) Solvency of the entity on balance date

Detail of Enhancement

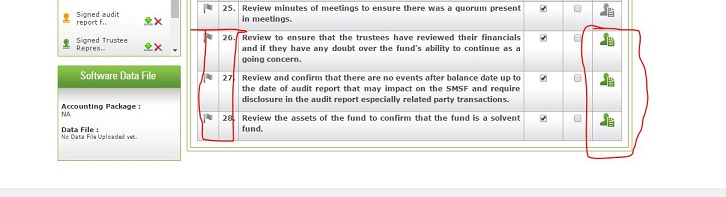

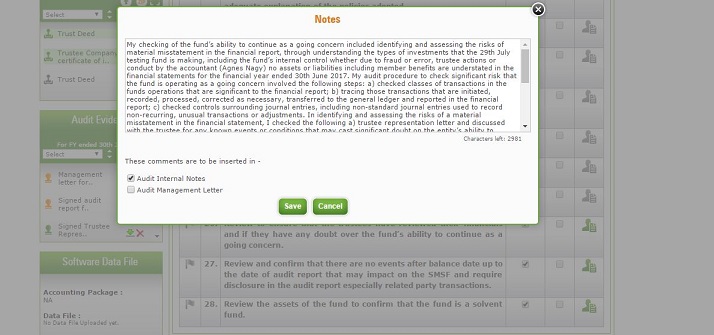

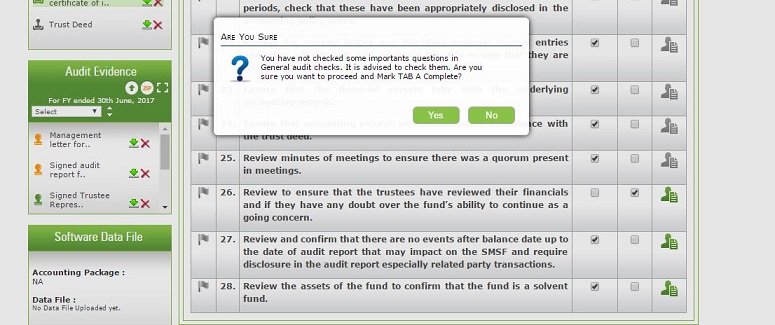

On Tab A under General Audit Checks - three new questions have been added.

If clicked Checked - we have provided Auditor default notes which can be changed. These notes will be automatically be included in the working papers if the box "Audit Internal Notes" is ticked.

If any of these three questions are not ticked as checked, the system will warn you as below. For those who do not use our system can incorporate these items in their audit program by clicking here.

Norwest SMSF Discussion Group

April 2017 Discussion Group

April meeting was held on 26th April and was attended by 34 SMSF professionals (mostly ASIC approved SMSF Auditors)

- click here to download presentation by Manoj Abichandani on pension rules from 1st July 2017

- click here to download presentation by Fred Walker on balance transfer cap from 1st July 2017

Next Seminar is on 30th May 2017 Wedneday - 5.30 PM to 7.30 PM

Next Discussion group meeting is on 30th May 2017 on "Estate Planning 101" from 1st July 2017"

Click here to see in detail what will be discussed in the meeting.

Introduction

If breaches of new lelgislation go unreported and ATO picks them up in their data matching process, negligent auditors can lose their licence. Auditors will need to be more vigilant and alert while auditing and more importantly posses "expert knowledge" as they will be called, more often, for their "audit opinion" on situations beyond the comprehension of a part time SMSF accountant (someone who administers less than 50 funds). These enquiries are likely to make the auditors role challenging & offcourse interesting.

Continuing professional development

There are very few SMSF auditor focused sessions on the new changes or seminars where auditors can update their knowledge. The challenge of new legislation is in the detail and many presentations are able to only scratch the surface.

Further, there is a Continuing professional development requirements that an approved SMSF auditor must complete, which is at least 120 hours of continuing professional development (CPD) training every three years, which must include 30 hours of training on superannuation of which at least 8 hours of training is about auditing of SMSFs. Time spent in this discussion group should be eligible for 1.5 hours in SMSF Audit under the self assessment method.

SMSF Auditors Discussion Group

CPD sessions in our office are on invitation basis on last Tuesday of every month. We send invitation to only ASIC approved SMSF Auditors in Bella Vista / Norwest Business Park and near by areas, we are delighted to invite you to the discussion group.

Date: 30th May 2017 - Tuesday

Agenda

5.30 PM Registration & Welcome Refreshments

6.00 PM Class Estate Planning 101 from 1st July 2017 - Speaker; Mr Manoj Abichandani

6.45 PM: Questions and Discussion on Estate Planning

7.00 PM Discussion: Changes to the requirements for obtaining an actuarial certificate

7.30 PM Close of Meeting

Venue: Nexus Cafe' Shop 1, 4 Columbia Court Baulkham Hills - Norwest Business Park

Cost: $25 (To Cover Refreshments & Room Hire Cost)

How to Register: www.onlinesmsfaudit.com.au/SeminarBooking.aspx

Seating: Maximum 40 -if you are interested in the topic, book as soon as possible.

Topic: Estate Planning 101

One of the greatest changes under the new super laws is arguably how transfer balance cap effects the payment of death benefits to spouses. This is because many members who exceed the cap can longer simply pay all of their death benefits to their spouse in the form of the pension. This means that careful planning is now required for members affected, or potentially affected, by the cap.

1.How the transfer balance cap works for death benefits?

2.Death benefit pensions vs reversionary pensions under the cap

3. When should existing pensions be converted into automatically reversionary pensions?

4.Dealing with the liquidity crunch on the death of the first spouse including in-specie death benefit payments

5.Implications for estate planning for TRISs

6. Child pensions – an opportunity or a trap?

7.Key issues, actions and strategies pre 30 June 2017

Speakers:

Manoj Abichandani SMSF Specialist (UNSW)

Manoj has been working in SMSF Space since 1988 in various capacities. Earlier he worked for a Specialist CPA firm as an advisor / accountant where he was responsible for 600 SMSF's funds, later he set up an audit firm where over 2,500 funds were audited each year which helped him to write Australia's first online audit software. At the time of writing over 58,000 funds have been audited on the online software and is the only online SMSF audit software where an SMSF auditor can save half his audit time.

Audit SMSF in Half Time - using our online Audit Tool

Where: Suite 3.04, Level 3, 29-31 Solent Circuit Baulkham Hills, NSW- 2153

Cost: $165 incl. GST

(Includes working Lunch / Coffee + 10 online audits worth $187 + 4 CPD Hours From FPA)

How to Register: Visit https://www.onlinesmsfaudit.com.au/SeminarBooking.aspx

Proposed Agenda

10.30 AM Registration - Arrival Tea and Coffee

11.00 AM Introduction to Audit Online on SMSF Audit Software

12.30 PM Lunch served during presentation

01.45 PM Coffee Break

02.00 PM Advanced SMSF Audit Issues and how to address them online

03.00 PM Workshop Closed

Introduction/Overview

SMSF Auditors spend too much time in financial audit and completing manual audit working papers, our online software does most of this work automatically & saves half your time as compared to traditional auditing methods. It checks closing share prices, dividends received from ASX and all mundane tasks of signing, scanning & mailing of audit report, Mgt. letter, engagement letter, Invoice & contravention reports etc. are automated with one click of a mouse.

Embrace an efficient framework for high quality audits and conduct audits on a flawless workflow Management system.

Achieve peace of mind & confidence of knowing that you are using a completely up-to-date online checklist and cloud process to deliver a robust, hassle free top quality SMSF audit. Improve communication with accountants & trustees. Manage 20 or 2000 audits by streamlining workflow from our smart Audit Manager & establish seamless communication between all parties. Our online SMSF audit system is the only tool which can deliver reliability, speed and volume and ultimately profits for your business at a fraction of the cost.

Benefits/learning outcomes

Audit from anywhere, anytime from any device on your own website or by integrating with ours. Increase audit effectiveness, add value, reduce audit risk, drive SMSF compliance, revolutionise your business.

Included in the fee is an account to audit 10 SMSF on the online platform worth $187 and Lunch & Coffee.

Those auditors who are already using the online software will benefit by learning new shortcuts and other advanced features of the online software.

Recommended For

All SMSF ASIC approved auditors.

CPD Hours

4 CPD hours under self assessment method under RG 243.88 - 90 for Audit of SMSF.

This activity has been accredited for continuing professional development by the Financial Planning Association of Australia but does not constitute FPA’s endorsement of the activity.

Accreditation number 008743 for 4 hours. Professional Dimensions Capability 2 Hours Professional Conduct 2 Hours - Knowledge Areas; 4 Hours SMSF

Attendee Requirements

Attendees may bring their own Laptops / Ipads for a better understanding - although some attendees may get more from the workshop by looking at the facilitators screen.

Manoj has worked in SMSF space for over 25 years, first as an SMSF specialist advising over 600 funds with a CPA firm and later as an SMSF auditor. He develops and lectures on strategies which are practical and enhances retirement benefits of trustees. He has been working for the last 6 years in writing and developing online SMSF audit software- Australia's first SMSF auditing tool.

.png)

When the use of the going concern basis of accounting is appropriate, assets and liabilities are recorded on the basis that the entity will be able to realise its assets and discharge its liabilities in the normal course of business.

When the use of the going concern basis of accounting is appropriate, assets and liabilities are recorded on the basis that the entity will be able to realise its assets and discharge its liabilities in the normal course of business. 2) Since any (or all) trustees can die at any time and their death benefit paid out compulsorily to beneficiaries, in particular Subregulation 6.21(1) of the SISR provides that a member's benefits in a regulated superannuation fund must be 'cashed' as soon as practicable after the death of the member (or the benefits are rolled over as soon as practicable for immediate 'cashing', in accordance with subregulation 6.21(3) of the SISR).

2) Since any (or all) trustees can die at any time and their death benefit paid out compulsorily to beneficiaries, in particular Subregulation 6.21(1) of the SISR provides that a member's benefits in a regulated superannuation fund must be 'cashed' as soon as practicable after the death of the member (or the benefits are rolled over as soon as practicable for immediate 'cashing', in accordance with subregulation 6.21(3) of the SISR).  What we have witnessed in the recent past is that reviewers from professional bodies insist that the SMSF auditor includes in his checklist audit procedures to check on the going concern capability of an SMSF. Auditors are being asked by reviewers to evaluate trustees procedure of examining the SMSF's going concern ability in the financial statements and design their own checklist and audit procedure to check if the financial statements are prepared under the going concern accounting framework and document these audit procedures in their working papers.

What we have witnessed in the recent past is that reviewers from professional bodies insist that the SMSF auditor includes in his checklist audit procedures to check on the going concern capability of an SMSF. Auditors are being asked by reviewers to evaluate trustees procedure of examining the SMSF's going concern ability in the financial statements and design their own checklist and audit procedure to check if the financial statements are prepared under the going concern accounting framework and document these audit procedures in their working papers.

.jpg)

SMSF Auditors spend too much time in financial audit and completing manual audit working papers, our online software does most of this work automatically & saves half your time as compared to traditional auditing methods. It checks closing share prices, dividends received from ASX and all mundane tasks of signing, scanning & mailing of audit report, Mgt. letter, engagement letter, Invoice & contravention reports etc. are automated with one click of a mouse.

SMSF Auditors spend too much time in financial audit and completing manual audit working papers, our online software does most of this work automatically & saves half your time as compared to traditional auditing methods. It checks closing share prices, dividends received from ASX and all mundane tasks of signing, scanning & mailing of audit report, Mgt. letter, engagement letter, Invoice & contravention reports etc. are automated with one click of a mouse.