A new document has been added on in www.trustdeed.com.au admin documents on "how to commute a pension on 30th June 2017" if your member balance is more than the balance transfer cap amount of $1.6 million, then any amount must be rolled back to accumulaiton phase.

This is a free document on our website, we have been advised that it is being sold for $299 on our competitions website.

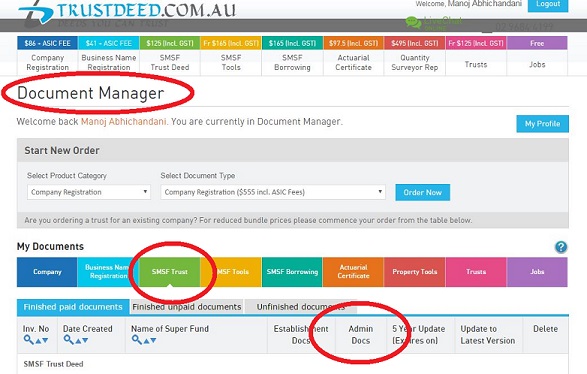

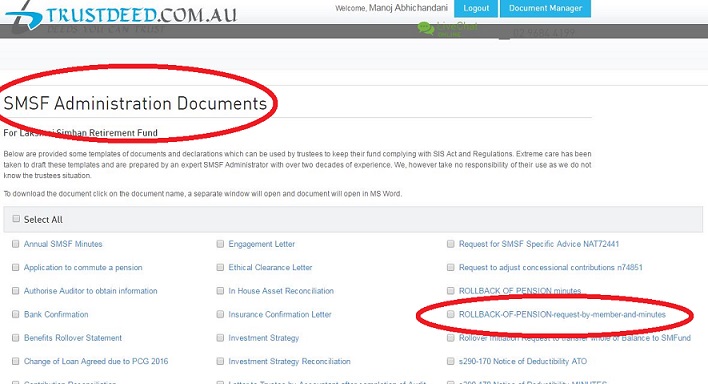

Step 1. To access this document, from document manager, click on green SMSF Trust and then click on "Admin Docs"

Step 2 Once you are in the Admin Docs - click on Rollback of Pension - to download the document.

How to commute a pension on 30th June 2017 to comply with Balance Transfer Cap

Any member of an Self Managed Super Fund (SMSF) who is in pension phase with balance above $1.6 million (transfer balance cap amount) on 30th June 2017, must either withdraw the amount above this amount from the SMSF or commute one or all pensions and move the amount from retirement phase to accumulation phase before or on 30th June 2017.

A member of an SMSF who is pension phase on 30th June 2017, may or may not have an accumulation account in that SMSF.

The actual commutation of the pension account to accumulation account is a mere journal entry to credit an existing or newly created accumulation account of the member in the fund and debit to one or more pension accounts of the member to ensure that the remaining pension account is not more than $1.6 million.

Income, tax calculations and asset valuation are generally not available on 30th June 2017, the trustees may need some time to quantify the amount above the $1.6 million as on 30th June 2017 in the pension account. Since trustees may not know the exact member pension balance on 30th June 2017, the exact amount of commutation from pension account to accumulation account may not be known for some time.

On 1st July 2017 not more than $1.6 million can be in retirement phase or else you will breach the transfer balance cap amount, commutation of pension of all amounts in excess of the transfer balance cap must happen on or before 30th June 2017.

For some SMSFs it is not possible to work out the pension balance on 30th June 2017, as valuation of some assets will not be known till much later. For example, units in unlisted or listed trusts are only known when the final accounts of the trust are completed sometime in September 2017.

ATO has put together a guidance to assist SMSF trustees with valuation of the pension where an SMSF member is unable to determine what their balance is at June 30 2017.

ATO in practical compliance guideline 2017/5 has suggested how these commutation requests from members should be recorded.

Trustees are not required to quantify the excess amount in the minutes they prepare for the pension commutation on 30th June 2017 but they need to be clear about how they intend to calculate the excess amount in the minutes, even though the amount of pension in excess is not determined much later than 1st July 2017.

This irrevocable request by the member and trustee accepting the request minutes must be in writing and must happen before 1st July 2017. These minutes must identify which income stream has to be commuted.

If you are an accountant and do not hold an AFSL, you cannot advice clients to set up SMSF's as the exemption for this advice is no longer available to you from 1st July 2016.

However, if a client instructs you, the legislation allows you to set up an SMSF as without advice, it is a simple administrative task. If these instruction come to you from your website, it is even better, as you can substantiate that no financial advice was provided by your firm.

We have launched a new website, www.smsfdeed.com.au which integrates with your website and anyone browsing your website can place an order / instruction with your firm to set up a new SMSF. When details are entered by the browser / new client on your website on an online form, they are actually filing our form which is integrated with your website . This way, you are not only able to establish an Audit trail that no financial advice was provided, but also when you log in to your account on our website, clients entered information is already waiting for you in the un-finished stage.

Our smart form can also create a new trustee company, if not already in existence and you can also apply for an ABN via our website for free, instead of re-keying the data on the government website.

This integration saves you time and effort to re-enter client information, all you have to do is edit the un-finished application, pay us and take delivery of a new SMSF deed and constitution of the trustee company. The cost of this service is $125 Incl. GST for individual or existing corporate trustee and $165 plus ASIC fees when a new corporate trustee has to be created as well.

For a demonstration on how this integration works, please visit www.diysuperfund.com.au. Integration requires your IT team to modify a few things on your website and then our IT team completes this integration.

The fee to integrate with our website is $660 Incl. Gst. For further information on how integration works,

Contact : Mrs Anjali Jatav

anjali@trustdeed.com.au

phone 0 2 9684 4199.

Free webinar on how to Integrate your website

Are you an accountant who wants to only do Accounting work for SMSF cleints?

Do you want to allow your clients to instruct you to set up an SMSF on your wesbsite?

Deed + Trustee Company + ABN = all in one form on your website in 2 days

Properties have varied investment returns, generally residential properties returns are lower as compared to commercial properties.

Members may want to retain properties with higher rental return in pension phase so that they can be exempted from tax. Any income and capital gain in accumulation phase is subject to 15% tax.

From 1st July 2017, you can no longer segregate pension assets from accumulation assets, all assets of the fund must remain un-segregated as that will be the members superannuation balance in the fund. An actuarial certificate will be required to determine exempt current pension income of the fund.

A person can be a member of multiple super funds. For example, if a member has two SMSF's, they may be able to achieve segregation between pension and accumulation assets. One fund up to $1.6 million could be in pension phase and the other fund can hold all the other assets in excess of $1.6 million and be in accumulation phase.

Fund with high return / income could then remain in pension phase and the pensions of the fund which has lower returns, such as residential properties, could be commuted to accumulation phase.

A second fund can be set up before 30th June 2017, however, SIS legislation does not allow rollouts of assets from one fund to another fund, unless where two funds are merging or in case of a marriage split. Rollovers of assets should not be confused with in-specie contributions where assets can be contributed to the fund, rollovers between two funds must always be in cash.

ATO has stated that they will be looking at applying provisions of Part IV A at situations where trustees are attempting to pull out or pull in assets from un-segregated pools to segregated pools . However, a genuine case where the trustee wants to set up one or two more funds for estate planning purposes should not be caught by these provisions.

SMSF as a Estate Planning Vehicle

If a member has more than one child, for estate planning purposes it can be beneficial to have one SMSF for each child, where the assets of the fund can pass on to the next generation without paying any capital gain tax.

These type of SMSFs typically will have three members, two parents and one child and once the child gets married, their spouse becomes the 4th member.

On death of one parent, the number of members will reduce and increase when a grandchild is admitted in the fund when he or she turns 18 years.

To implement this strategy parents should be gradually drawing down on pensions and gifting it to the child who will then contribute to the fund as non-concessional contribution, so that one day parents are phased out of the fund and kids (plus spouse) member balance represent the assets of the fund.

This strategy works to eliminate or limit capital gain tax when the asset is ultimately sold, presumably when the child or grandchild is in pension phase.

Investments making a gain and held outside of super will always pay capital gain tax, however this strategy can be used by multiple generations, as an SMSF can go on till perpetuity.

This similar capital gain tax shelter is only currently available on sale of principal place of residence i.e. on death of a parent, any capital gain on the sale of principal place of residence passes to the next generation without any capital gain tax liability. The cost base of the deceased for each investment property passes to the beneficiary at the time of death and capital gain tax paid on its ultimate sale.

Having one SMSF for each child strategy ensures that assets move from one generation to the next without paying any or minimal capital gain tax on the assets ultimate sale with the advent of transfer balance caps which restricts the amount which can be in pension phase.

If you or your clients have only one fund and want to set up another fund (or funds) for estate planning purposes before 30th June 2017 and divide the assets of the current fund by moving some properties to the new fund, there is a further restriction imposed by exemptions contained in Section 66 of SIS Act.

Only business real property (BRP) can be acquired from a related party, the two funds would be considered to be related to each other and transfer of any residential property will be prohibited.

If BRP of one fund has to be moved to another fund, you will first have to rollover cash from one fund to the second fund so that trustees of the second fund are able to purchase BRP from the trustees of the first fund. Since the first fund is in pension phase, this sale will trigger a CGT event, however no tax will be payable as there is no capital gain tax on sale of assets which are 100% supporting a pension before 1st July 2017.

When BRP is sold to another SMSF, the beneficial interest in the property will remain the same as the property will move into the new fund for the same members, albeit in another fund, no stamp duty should be payable. Enquiries should be made with the office of state revenue before implementing this strategy.

Many investors are withdrawing the excess over the balance transfer cap amount and investing outside of super in structures like family trusts.

SMSF Auditors spend too much time in financial audit and completing manual audit working papers, our online software does most of this work automatically & saves half your time as compared to traditional auditing methods.

Achieve peace of mind & confidence of knowing that you are using a completely up-to-date online checklist and cloud process to deliver a robust, hassle free top quality SMSF audit. Approved by many professional body reviewers (list provided).

All mundane tasks of signing, scanning & mailing of audit report, Management letter, engagement letter, Invoice & contravention reports etc. are automated with one click.

Manage 20 or 2000 audits by streamlining workflow from our smart Audit Manager & establish seamless communication between all parties.

Embrace an efficient framework for high quality audits and conduct audits on a flawless workflow Management system.

Meet or exceed legislative & professional requirements…

Keep ahead of the competition...

Try before you buy

Online SMSF Audit offers you a risk-free chance to try the software without purchasing.

No credit card required to register. Your account will use the full version of the software and will be credited to audit five funds for free.

There are no feature limitations to the trial version! To continue using the software after trial 5 funds, purchase a single license to audit your 6th fund or purchase a discounted bundle pack. Simply follow the easy steps below to utilize the trial.

You are just seconds away from discovering why Online SMSF Audit is the leading audit solution for large and small SMSF auditors.

Increase audit effectiveness, add value, reduce audit risk, drive SMSF compliance, revolutionise your business. Welcome to the world of cloud auditing...

Be a better auditor, you have the knowledge we have the tools

Our online system is your solution....get in, early...

.png)

A member of an SMSF who is pension phase on 30th June 2017, may or may not have an accumulation account in that SMSF.

A member of an SMSF who is pension phase on 30th June 2017, may or may not have an accumulation account in that SMSF.  For some SMSFs it is not possible to work out the pension balance on 30th June 2017, as valuation of some assets will not be known till much later. For example, units in unlisted or listed trusts are only known when the final accounts of the trust are completed sometime in September 2017.

For some SMSFs it is not possible to work out the pension balance on 30th June 2017, as valuation of some assets will not be known till much later. For example, units in unlisted or listed trusts are only known when the final accounts of the trust are completed sometime in September 2017. However, if a client instructs you, the legislation allows you to set up an SMSF as without advice, it is a simple administrative task. If these instruction come to you from your website, it is even better, as you can substantiate that no financial advice was provided by your firm.

However, if a client instructs you, the legislation allows you to set up an SMSF as without advice, it is a simple administrative task. If these instruction come to you from your website, it is even better, as you can substantiate that no financial advice was provided by your firm.

Properties have varied investment returns, generally residential properties returns are lower as compared to commercial properties.

Properties have varied investment returns, generally residential properties returns are lower as compared to commercial properties.  If a member has more than one child, for estate planning purposes it can be beneficial to have one SMSF for each child, where the assets of the fund can pass on to the next generation without paying any capital gain tax.

If a member has more than one child, for estate planning purposes it can be beneficial to have one SMSF for each child, where the assets of the fund can pass on to the next generation without paying any capital gain tax.  If you or your clients have only one fund and want to set up another fund (or funds) for estate planning purposes before 30th June 2017 and divide the assets of the current fund by moving some properties to the new fund, there is a further restriction imposed by exemptions contained in Section 66 of SIS Act.

If you or your clients have only one fund and want to set up another fund (or funds) for estate planning purposes before 30th June 2017 and divide the assets of the current fund by moving some properties to the new fund, there is a further restriction imposed by exemptions contained in Section 66 of SIS Act..jpg)

.png)