Understanding TBAR: Reversionary vs Non- Reversionary Pension

News | Mehak gaba |Released: 02/07/2025 | Read: 5 Mins

When a member of a super fund passes away with an ongoing account-based pension, what happens next largely depends on how the pension was structured at the time it commenced?

Superfunds allow members to nominate a reversionary beneficiary — usually a spouse or dependent- who will automatically continue to receive the pension after the member’s death. with no disruption. This is called a reversionary pension. It’s simple, automatic, and the pension doesn’t stop.

If you didn’t make a reversionary nomination, or the nomination is invalid, the pension ends when the member dies. The remaining balance is then paid out as a death benefit, either as a lump sum or a new pension, depending on what instructions (like a Binding Death Benefit Nomination or BDBN) were in place. This is called a non-reversionary pension.

The key difference between the two is not just how the pension continues — but also how it's reported to the ATO (through TBAR) and when and how it affects the person receiving it under their Transfer Balance Cap (TBC).

From 1 July 2025, the TBC (which limits how much you can have in a tax-free retirement pension) will increase to $2.0 million. This cap applies to the person receiving the pension, and the timing of when it counts depends on whether the pension is reversionary or not.

🔁What is TBAR and the Transfer Balance Cap?

🔁What is TBAR and the Transfer Balance Cap?

TBAR (Transfer Balance Account Reporting) is a report that super funds must send to the ATO to let them know when a person starts receiving a pension — including after someone’s death.TBAR Events Include starting a new retirement phase income stream (pension), Commuting (partially or fully stopping) a pension and receiving a death benefit pension (reversionary or non-reversionary).

Transfer Balance Cap (TBC) is the maximum amount a person can have in tax-free retirement income streams (like an account-based pension). Anything above the cap must remain in accumulation phase (taxable earnings) or be withdrawn.

➕For Reversionary Pensions:

The pension amount is counted against the beneficiary’s cap 12 months after the original member’s death. This delay gives the beneficiary time to adjust if needed (for example, by commuting part of the pension) to avoid exceeding their cap.

➕For Non-Reversionary Pensions:

The pension amount is counted immediately when the new pension starts, and includes any growth in value since the member died.

This timing difference can make a big impact on tax planning and how much a beneficiary can keep in a pension. That’s why it's so important to understand the difference and plan accordingly.

Reversionary Pension (Automatic Continuation to Spouse/ Dependants)

1. Minimum pension requirements: Even after the original pensioner passes away, the reversionary pension must still comply with the minimum pension payment requirements set by the ATO for the financial year.

For example, if John passed away in October 2025, and had already received $10,000 of a $30,000 minimum, the remaining $20,000 must be paid to the reversionary beneficiary (e.g., his spouse) before 30 June 2026. The obligation shifts but doesn’t reset.

2. Pension is Deemed to Continue from the Date of Death: The pension does not stop at death — it is legally deemed to continue uninterrupted, transferring to the reversionary beneficiary from the date of the member’s death.This date is important for Transfer Balance Account Reporting (TBAR), as it determines when the value is assessed for the 12-month deferral period before being counted toward the recipient’s Transfer Balance Cap (TBC).

3. Nomination is Ongoing – No Renewal Required: Unlike some non-binding death benefit nominations that may lapse after three years (depending on the fund’s rules), a valid reversionary nomination made at the commencement of the pension does not expire or require renewal. It remains in place unless the pension is commuted or restructured entirely.

4. Legally Binding on the Trustee: Once a valid reversionary nomination is in place, the trustee has no discretion — they must continue paying the pension to the nominated reversionary beneficiary. This legal certainty can help reduce delays, disputes, or confusion during what is already a difficult time for the family. Because of its binding nature, reversionary pensions are rarely subject to challenge compared to death benefit nominations.

5.The Reversionary Beneficiary Becomes the New Pension Holder: The reversionary beneficiary acquires beneficial ownership of the pension and gains similar rights to the original pensioner (subject to fund rules).

This includes powers to:

Change investment options within the SMSF.

Alter payment frequency or amounts (within minimum limits)

Fully commute the pension as a lump sum, if desired or any other powers as original pensioner holds.

However, the pension cannot be reverted back to accumulation phase, as it remains a retirement-phase income stream under superannuation law.

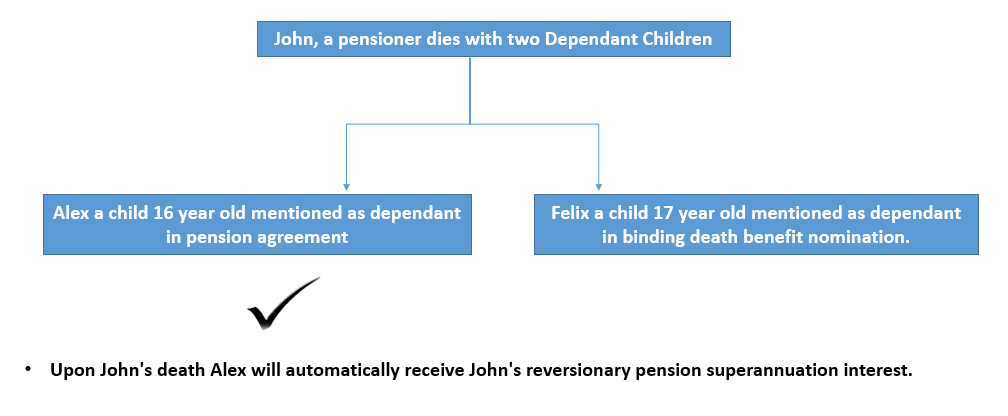

Important Tip: It's critical that your SMSF deed clearly outlines how reversionary pensions interact with death benefit nominations. In practice, members may have:

A reversionary beneficiary nominated in the pension agreement

A Binding Death Benefit Nomination (BDBN) specifying someone else

If the deed isn’t clear, this can lead to conflicting instructions, legal disputes, and delayed payments to beneficiaries.

In case of Conflicts- Who gets priority? Reversionary Vs Other Nominations

Your SMSF’s governing rules should clearly outline how to handle death benefit payments, particularly where both a reversionary pension nomination and a binding or non-binding death benefit nomination exist.

At Trustdeed.com.au, we’ve addressed this issue directly in our deed. As per Clause 169 of our SMSF Deed, it is clearly stated that:

“Where there is any inconsistency between the reversionary beneficiary named in the pension agreement and the person nominated in a binding or non-binding death benefit nomination, the reversionary nomination will take precedence.”

Non Reversionary Pension- Trusted Directed Payment After Death

1. No Minimum Requirement for Year of Death: Since the pension ends at death, the fund is not required to meet minimum pension standards for the deceased member.

2. General Priority Order for Payments:

First: Binding Death Benefit Nomination (BDBN)

Second: Non-Binding Nomination

Third: Trustee discretion for eligible dependants under super law

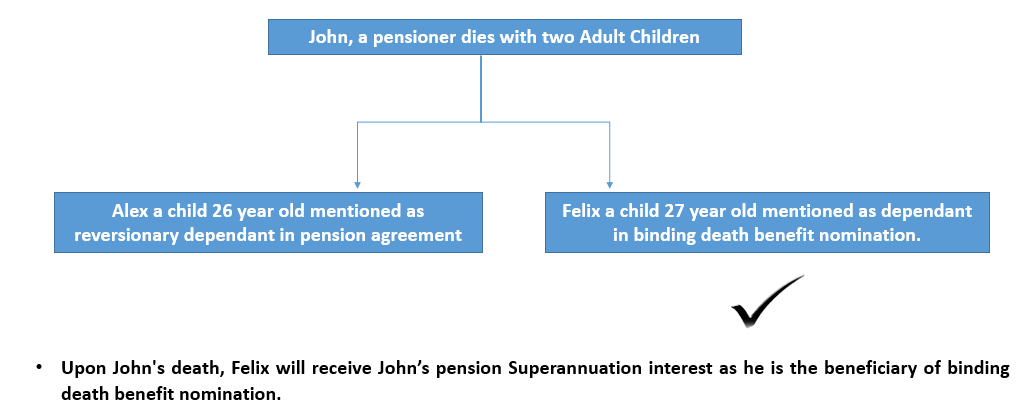

Important: Pensions can only be paid to dependants. Non-dependants (e.g., independent adult children) must receive lump sums. If the deed isn’t clear, this can lead to conflicting instructions, legal disputes, and delayed payments to beneficiaries conflicting instructions.

In case of conflicts-Who gets priority?

Reversionary vs Other Nominations

If there’s a conflict between:

Someone named in the pension agreement as a reversionary, but who can’t receive a pension (e.g., an independent adult child), and;

Someone named in a Binding Death Benefit Nomination, who also can’t receive a pension,

Then the person named in the Binding Nomination will get the lump sum, even if they were not mentioned in the pension documents.

At Trustdeed.com.au, we’ve addressed this issue directly in our deed. As per clause 170 of our SMSF Deed, it is clearly stated that:

“When both the reversionary beneficiary (in the pension agreement) and the binding death benefit nominee are ineligible to receive a pension under super law, an inconsistency arises then the binding death benefit nomination (BDBN) takes priority for the payment of the deceased member’s super interest as a lump sum.”

Join my webinar on 23th July- Accumlation to Pension: ABP, TRIS & other choices

Register now! Expand your knowledge! You are warmly invited to join my webinar and earn CPD hours!

❓Can a Pension Be Paid to a Non-Dependant (e.g. Adult Children)?

Answer: No – never.

Under superannuation law, pensions can only be paid to eligible dependants (like a spouse, financial dependants, or those in an interdependency relationship).

If a non-dependant is nominated (e.g. an adult child who is not financially dependent), they must receive a lump sum, not a pension.

❓No Dependants – Who Gets the Super?

Situation:

James had no spouse or financially dependent children. He was receiving a non-reversionary pension and left no valid Binding Death Benefit Nomination (BDBN) at the time of death.

Question:

How should the trustee distribute his remaining super balance?

Answer:

⚖️ The trustee cannot pay a pension, as there are no eligible dependants.

Instead, the benefit must be paid as a lump sum, either to:

James’s legal personal representative (LPR) (i.e. his estate), or

A non-tax dependant (e.g. adult child), at the trustee’s discretion.

❓TBAR & TBC Timing – Non-Reversionary Pension

Situation:

John passed away with a non-reversionary pension. His Binding Death Benefit Nomination directed the trustee to pay the balance as a new pension to his spouse, Leena. The trustee commenced the pension within a month of his death.

Question:

When will the amount count toward Leena’s Transfer Balance Cap (TBC)?

Answer:

📅 Immediately when the new pension starts.

There is no 12-month deferral like with reversionary pensions.

Leena’s TBC will be debited the full value of the pension, including any earnings accrued from John's date of death to the pension start date.

✅ Action Points for Advisors and Trustees

1. Review trust deeds and nominations. Ensure the SMSF deed allows reversionary pensions and that any intended beneficiaries are properly nominated. Relevant documentation completed to indicate your nomination at the commencement of the pension.

2. Discuss objectives with clients. If clients want their spouse guaranteed an income stream, a reversionary pension may be best. If they need flexibility (e.g. including children or charities), consider a non-reversionary strategy with binding nominations.

3. Lodge TBARs promptly. Whether reversionary or not, lodge the TBAR within the required timeframe (28 days after notification) for any death benefit income stream start.

4.Use the 12-month window: reversionary pensioner as being in receipt of the pension from the date of the primary pensioner’s death With a reversionary pension, this window of 12 months is an opportunity to restructure and avoid excess transfer balance issues. Be careful though, it will count automatically after that, so if this will cause a breach of the member’s transfer balance cap, it should be dealt with within the 12-month period.

5.Monitor Transfer Balance Caps. Check each member’s existing TBC usage. Remember the $2.0 million cap from 1 July 2025 and plan accordingly. If a reversionary pension would push a beneficiary over the cap in a year, plan a partial commutation now.

6. Be Aware of Relationship Changes: If a member divorces or separates from their reversionary beneficiary, they may need to commute and restart the pension, potentially incurring administrative and tax costs.

Visit www.trustdeed.com.au for more details or call us on(02) 9684 4199

.jpg)